Big Yields and Free Crypto With DeFi

Dear Frontier Fortunes Subscriber,

How do these returns strike you: 15%... 10.21%... 9.19%... 8.75%... 10.3%... 17.5%.

Oh, and those are annual returns.

And they’re on cash—good ol’ US dollars put to work on your behalf. Only, it’s crypto cash.

For comparison, the highest return on cash I found in a “trad bank” while writing this issue of Frontier Fortunes was 4.25% on a 13-month certificate of deposit at Hyperion Bank in Philly.

High returns on cash, you might guess, is what this quarter’s issue is all about.

More broadly, it’s about the ways in which decentralized finance, or DeFi for short, is showing us the future of banking… today.

We’re not going to be chasing moonshot gains here, but we are going to be chasing high yields on idle dollars. And along the way, we might actually collect some free money from airdrops.

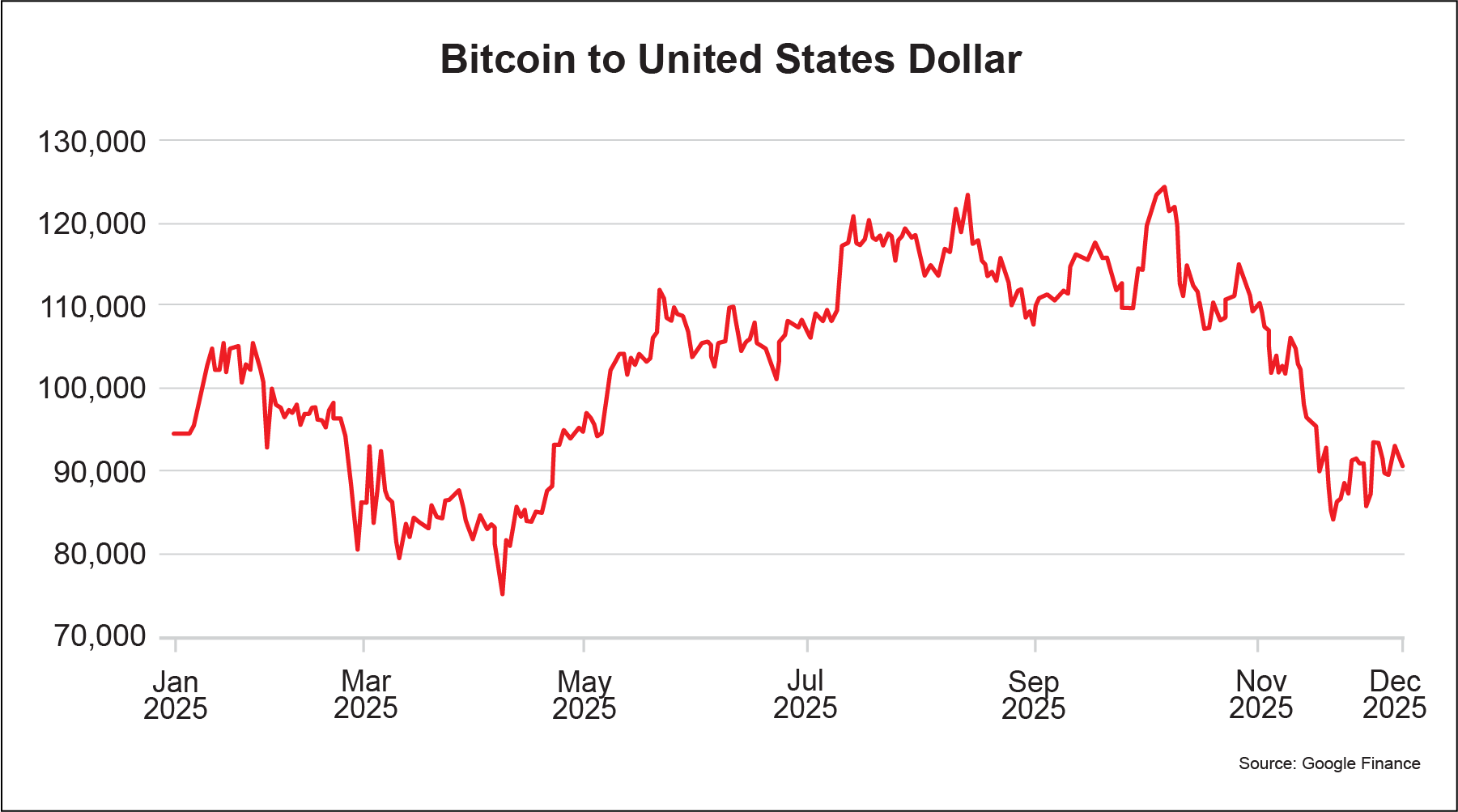

But before we dive into all of that, I want to offer some insight on the volatility we’ve seen recently in crypto. The year started out bright with much promise. But along the way, countervailing forces have intruded and they’ve recently driven crypto prices down.

Know this: The downdraft is temporary.

The sell-off recently in bitcoin, Solana, Ethereum, and others has nothing to do specifically with those projects or crypto in general. Rather, it has everything to do with those countervailing forces.

So, with that as our preamble, let’s dive in and address those forces… and then, let’s go earn some big, safe return on our cash.

As I noted, 2025 began with great promise for crypto.

The market was in a bull phase. A new administration was heading to the White House, and it was clearly promising to be a crypto-friendly government. Corporations and the financial industry were moving heavily into crypto after years of panning digital currency.

And one of the biggest thorns in the industry’s side, SEC Chairman Gary Ginsler, stepped down, and a crypto-friendly chairman, Paul Atkins, took control. One of his primary missions: A regulatory framework under his “Project Crypto” banner that aims to foster innovation in crypto that will ultimately lead to the tokenization of pretty much all assets.

Basically, he’s saying that we’re moving to a world where stocks, bonds, currencies, real estate, collectibles, mutual funds, and pretty much everything else of value will be trading on the blockchain as digital assets.

So, all of that was brilliant for the industry.

But then there’s the flipside of the Trump administration…

To be sure, Trump is an outspoken proponent of crypto. And his talk of a bitcoin reserve fund for America, and turning America into what he called “the capital of crypto,” saw bitcoin rise nearly 50% in a single month after his election win last year.

Unfortunately for the industry, Trump is also a fan of tariffs. And the economic strategy of attacking global trading partners has not set well with the US economy. Which means it hasn’t set well with crypto, which is highly sensitive to economic flows.

In Trump’s first three months in office this year, when all he did was badmouth trading partners including America’s most-important friends, bitcoin fell nearly 30%.

As Trump then struck a series of one-off deals with individual nations, and as his rhetoric toward China moderated—and as his outrageously boneheaded tariff levels of multi-hundreds of percent fell back toward normal levels—crypto rallied once again.

The belief was that the world was returning to some kind of acceptable abnormal.

That set bitcoin racing up nearly 64%, to a new all-time high approaching $125,000 in early October.

Then… Tariff J. Trump struck again.

Miffed that China wasn’t playing his game, and angered that the Chinese had the temerity to impose bans on the rare-earth metals the country produces and which American industry desperately needs, Trump threatened to slap a new 100% tariff on China.

Bitcoin promptly fell out of bed again, losing more than 30% in just six weeks.

Clearly, then, Trump’s misguided policy of punishment-by-tariff is slamming crypto.

Bitcoin—and the broader crypto market—has risen and fallen this year with news and announcements on tariffs and the wider economy.

Separately, a Japanese issue has emerged.

Last year, the Bank of Japan announced it would begin normalizing interest rates after 30 years of failed financial engineering that kept rates in Japan on the floor. The country has raised rates three times since 2024, and the markets haven’t really freaked out.

But inflation has run persistently high in Japan, despite the rate hikes. And on December 1, Japan’s central bank hinted at a more hawkish stance. The problem: For 30 years, the Japanese yen has been at the center of something called the “carry trade.” In a nutshell, that’s a strategy of borrowing and immediately selling low-yield assets (such as the yen) and putting the proceeds to work in high-yield assets (such as stocks and crypto). In doing so, the trader is paying the low-yield while collecting the high-yield. The spread between those two rates is the profit, and it’s generally been pretty easy money.

With yen rates on the rise, however, that disrupts the carry trade, which hits the money flowing into crypto.

All of that—Trump’s tariffs and the yen carry trade—have nothing to do with the fundamentals of crypto.

They have to do with the fact that financial markets—especially crypto—work on fear and greed.

That in itself is frustrating for anyone who has grown up investing in the stock market. It too operates along a fear/greed continuum, but the stock market is much more mature and quality stocks tend not to move as dramatically or as quickly as crypto does.

The crazy moves in crypto too often drive investors out of the market at just the wrong moment.

Indeed, near bitcoin’s recent bottom around $84,000, I was seeing all kinds of comments on Twitter/X from traders exclaiming “I’m out!” or “I can’t take this anymore” or “this is the worst bull market I’ve ever seen—I’m leaving.”

Since then, bitcoin is back up about 10%.

That’s largely because the latest China tariff threat never materialized, and because of increasing expectations that America’s Federal Reserve will be forced to cut interest rates to save a US economy that’s teetering due to tariffs that have exacerbated inflation, hurt the consumer, and are leading to vast job losses across multiple industries.

Low rates encourage investors to chase risk in pursuit of return, which is great for crypto because it’s among the riskiest of risk-on assets.

All of that, however, is just noise.

“The fundamentals in crypto are actually stronger today than they were at the beginning of the year.”

The overlooked reality is that the underlying fundamentals in crypto are actually stronger today than they were at the beginning of the year.

Banks such as Pittsburgh’s PNC have partnered with crypto-exchange giant Coinbase to soon begin offering bank customers a convenient way to buy, sell, and hold crypto through a traditional bank account. At least 15 US states now hold bitcoin exchange-traded funds inside their state pension plans. Harvard’s massive $52 billion endowment now has a bitcoin ETF as its largest stock market holding.

And at least 163 institutions globally now officially hold more than $157 billion worth of bitcoin, representing more than 8% of the entire bitcoin supply.

Even longtime crypto curmudgeon Jamie Dimon, head of JPMorgan Chase, recently announced that crypto is the future of finance, especially when it comes to banking efficiency.

As I said, the underlying fundamentals are actually improving, even as exogenous events conspire to (temporarily) push down crypto prices.

That will change. Guaranteed.

And when it does, prices for bitcoin, Solana, Ethereum, and many others are going to reclaim their upward trajectory, and all are going to see new all-time highs that are substantially higher than today.

In the meantime, we can earn a nice bit of return on crypto just by putting USDC and other stablecoins to work…

As their name implies, they’re cryptocurrencies that are designed to be stable, meaning they’re not going to bounce around violently like bitcoin and others.

Stables such as US Dollar Token (USDT, or Tether) and US Dollar Coin (USDC) track the real greenback on a 1:1 basis. The fluctuation that happens is fractions of cent. But for all intents and purposes, you never see that in your account.

If you send $100 to your account at a crypto exchange such as Coinbase, Kraken, Gemini or wherever, and you buy 100 USDC, your fiat dollars convert into the exact same amount of dollar-based stablecoins.

And when you convert your 100 USDC back into fiat, you’re going to get $100 that you can then send to your real-world bank, where a $100 credit will appear.

So USDC and USDT are stable.

But they’re not the only dollar-centric stablecoins that exist.

PayPal, for instance, has its own stable known as PYUSD. World Liberty Financial USD (USD1) is a stable tied to a Trump-based crypto venture. Gemini USD is tied to the Gemini crypto exchange. It goes on and on.

Each one has some form of income opportunity somewhere within the world of decentralized finance, or DeFi, as it’s more commonly called.

DeFi is basically everything you can do with money and investing in real life, just executed on the blockchain.

Bank savings accounts, buying stocks, owning exposure to real estate, buying collectibles… all of that is available through the crypto market by way of DeFi websites.

But DeFi is so much more. Individual investors have the opportunity now to invest in areas that have never before been available to a retail marketplace.

Take reinsurance, for example.

Insurance companies all over the world buy their own forms of insurance—reinsurance—just in case a catastrophe like a hurricane is so large that the original insurer would be devastated by claims.

Well, on the blockchain, I’m actually in a crypto project called OnRe. It’s a regulated blockchain-based reinsurance company linking the traditional, multibillion dollar reinsurance market with investors operating in decentralized finance. That could very well be large institutions… or small-fry like me.

We both get to put our money to work in a very stable market, reinsurance, and for doing so, we’re sharing in the insurance premiums that OnRe collects. By owning OnRe’s ONyc token, which is a yield-bearing crypto asset, I’m collecting a 13.5% yield.

Those kinds of income opportunities exist all over DeFi today.

Which is why the DeFi space has exploded in size. From roughly $21 billion worth of assets invested in DeFi in 2021, the space is now north of $120 billion. Estimates have it eclipsing $500 billion before the end of the decade as increasing numbers of business and retail investors discover the opportunities for fat returns that they’re currently missing out on.

Though the Ethereum network remains the biggest pool of DeFi money at more than $70 billion, Solana is #2 ($10 billion) and growing substantially faster than Ethereum. That’s because Ethereum’s network is slower than a three-legged turtle walking backways through a pool of molasses. Moreover, Ethereum’s per-transaction costs are roughly $0.20 to $0.35, but can spike into the dollars when the network is congested… and network congestion is frequent because ETH can process just 17 or so transactions per second.

By comparison, Solana’s network consistently runs at 4,000 to 6,000 transactions per second (Visa and Mastercard run the credit-card world at just 1,700 per second), and an upgrade coming to Solana has already demonstrated consistent speeds of 1 million transactions per second. So there’s little chance of meaningful congestion.

Moreover, transactions on Solana cost, on average, $0.00025, with some DeFi transactions costing upwards of $0.003. To put that into perspective, a DeFi investor on Solana could executive roughly 100 transactions for every one transaction on Ethereum.

For that reason, most of the new and innovative DeFi opportunities are now emerging on Solana, which is where we are going to focus on collecting some income from stablecoins.

I won’t burden you with multiple strategies at multiple DeFi sites because once you understand a few of them, you can begin to extrapolate and experiment with strategies at any of the many DeFi sites across the Solana blockchain.

Before we begin, a note: You’re going to want to use a browser for these opportunities. You’re not going to access them through a centralized crypto exchange such as Coinbase, Binance.US, Kraken, or others.

Instead, you will need a browser wallet that runs on the Solana blockchain. I use Phantom, Solflare, and Backpack. All are easy to set up, but if you need a refresher on how to do that, read this report on how to use a browser wallet (start on page 27).

Perena is a DeFi protocol tied to a yield-bearing stablecoin, called USD* or USD STAR, that’s pegged to the US dollar and collateralized by various assets including short-term US Treasury bills managed in partnership with financial services giant Franklin-Templeton.

In the crypto context, a “protocol” is essentially a set of rules and instructions that “smart contracts” implement on a given blockchain. In this case, we’re talking about the Solana blockchain. As for smart contracts, they’re simply a set of instructions, written in computer code, that execute independent of human intervention or a central authority once all the necessary parameters fall into place.

The best analogy I can think of is a vending machine.

At its simplest, a vending machine is a self-contained system with a fixed set of rules: Insert the correct amount of money, press the button for a specific item, and the machine automatically dispenses that item without having to seek approval from a central authority.

It’s exactly the same with a DeFi protocol: Deposit a given asset, select a given investment or strategy, and the smart contract guiding the protocol does all the work on the backend to execute your selection without checking in first with a central authority.

And just like a vending machine, DeFi protocols run 24/7/365. Moreover, no one can change the rules on a whim. DeFi protocols are fixed in place once the “machine” is set to run.

As for Perena and collecting 15% on a dollar-based stablecoin, this is a protocol that generates yield primarily through a combination of passive and active strategies applied to the stablecoins you deposit.

The protocol aims for sustainable, risk-adjusted returns. That doesn’t mean there’s no risk—there’s always some kind of risk, even with stablecoins. But Perena’s protocol design mitigates this through diversification and other means. (I’ll explain the risks in a moment.)

Perena’s yield, which fluctuates between 10% and 15% or so based on market conditions, comes from fees it generates as well as trading strategies it uses, and which are designed to be market neutral (i.e. lead to a return regardless of whether the market is up or down). I won’t go into the mechanics of it all because it’s deeply inside baseball and deals with crypto terms such as “automated market maker,” “total value locked,” “liquidity provider” and such, and I really do not want to lull you into a nap.

Instead, I’ll tell you to think of Perena as a high-tech, high-yield savings account.

You first deposit a stablecoin such as US Dollar Coin, known as USDC, into a big, shared pool of stablecoins at Perena’s website. When you deposit your USDC, you receive Perena’s yield-bearing USD* stablecoin as a claim on your share of that big pool. This isn’t precisely a 1:1 transfer, but it will be fairly close. So if you deposit 100 USDC (equal to $100 fiat USD) as I write this, then you will receive about 97 USD*.

Perena then uses that big pool to generate income in several ways.

The income that Perena generates lands in your account in the form of additional USD*, and that USD* starts earning yield as well—the process of compounding, just like interest on a savings account starts earning interest too.

As I noted, the income-generating strategies aim to offer yields of between 10% and 15% based on market conditions. When I first deposited USDC into Perena, I was earning 14.92%. That jumped to 15.01%, and is currently at 14.90%.

How to Put Money to Work With Perena

Buy USDC at Coinbase or whatever crypto exchange you use.

Send your USDC to your browser wallet. (Remember, you’ll find a refresher on browser wallets here.)

Connect your browser wallet to the Perena app. Be sure you have a little bit of Solana in your wallet, since you will need that for transaction fees… 0.1 SOL, or about $13 as a write this, will be more than enough. (Note: the links I am sharing with you are my personal referral links because sometimes you need a referral from an existing user to gain access; sometimes you get a bonus; and because I want to ensure that you absolutely end up at the right website to avoid any kind of scam links, since those are everywhere in crypto. It never adds to your cost in any way. But just to be totally upfront: I may ultimately see some benefits if you choose to use these links. It’s a win-win!)

Click on “Get USD*”.

Under “Amount,” chose how much USDC you want to invest and follow the prompts.

You will end up with USD* equal to the amount of USDC you invest. You’ll see your deposit under the “Portfolio” link at the top of the page.

That’s all you have to do. USD* will accrue to your account automatically, and you will see that daily in the “Yield Earn” section.

The Risks With Perena

As a stablecoin, USD* isn’t designed to shoot the moon, like other cryptocurrencies. Which means it’s also not likely to slump to zero. But there are certain risks to be aware of.

First, Perena is not a bank and your deposit is not FDIC insured.

The potential risks you face are:

In theory, you could lose everything you invest. But that risk is small, given the assets in the big pool are dollar-based stablecoins. A complete meltdown would require a catastrophic smart contract exploit, full depeg of all underlying stablecoins, or cascading strategy failures across the entire protocol.

Perena's design, however, mitigates the risks through diversification, active management, and other methods.

A Potential Airdrop Windfall

Aside from the plump yield, one of the reasons I’ve put money to work at Perena is the potential for an airdrop—free tokens that land in your wallet simply because you are a user of the platform.

Airdrops I have been a part of over the years have carried values of roughly $700 to more than $36,000. I can’t say where Perena might fall in that mix.

Nor can I say with certainty that Perena will, in fact, pursue an airdrop. However, deposits of $100 or more earn “Petals” every day, which is basically a points system. And DeFi protocols running points systems have historically led to airdrops. So I’m investing to earn yield, and to collect a potential airdrop, if it happens.

Loopscale is a decentralized lending protocol on the Solana blockchain that matches those who want to borrow money with those who have money to lend.

In this case, all the borrowing/lending happens on the blockchain, without any central oversight, and the loans are overcollateralized by between 150% and 300%. That gives lenders a lot of headroom in case the market turns sour.

The 8.68% yield comes by way of the interest rates that borrowers are paying to access lending on Loopscale.

And because of loan-maintenance thresholds, the smart contracts governing the position automatically liquidate the loan if the value of the collateral falls far enough. In that instance, the borrower loses out and the lender is made whole, including principal plus accrued interest.

It’s really as simple as that.

How to Put Money to Work With Loopscale

With your USDC already in your browser wallet, just connect to Loopscale’s website.

Select the “USDC Genesis” option by clicking the Deposit button.

On the right, look for the Deposit / Withdraw dialog box. Select how much USDC you want to deposit, and click Deposit.

You’re done.

Note: Loopscale limits the amount of assets in its pools, or what Loopscale calls “vaults.” So where you would normally see Deposit when initially selecting the USDC Genesis vault, you might see “Supply limit reached.” If so, you will not be able to make a deposit until someone else withdraws. So just keep checking back daily until a vault opens up.

The Risk With Loopscale

Aside from a catastrophic hack or smart-contract failure, there’s really no meaningful risk.

The overcollateralized-loan design means that the worst-case scenario would involve a partial principal reduction from extreme bad debt in a “flash crash” that evades the liquidation parameters. But that’s quite the small risk.

Yields could go to zero temporarily, in some rare instance, but your principal remains protected by those collateral buffers.

Another Potential Airdrop Windfall

As with Perena, Loopscale is running a points system at the moment, based on how much lending and borrowing volume you do, as well as how much “looping” volume you do (I’ll explain looping next).

Expectations are that the airdrop happens next year, and that the token might be a yield tied to “staking.” That means those who stake, or deposit, their tokens at the Loopscale site might earn part of the revenue that Loopscale generates. None of that is set in stone, of course, but I’m participating in Loopscale just in case.

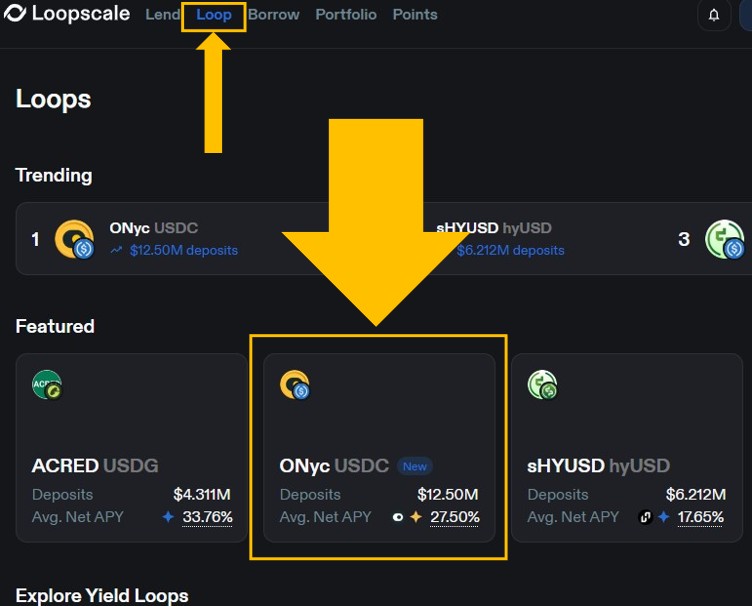

I mentioned OnRe earlier—the regulated, blockchain-based reinsurance company.

OnRe’s flagship token is known as ONyc, a yield-bearing, multi-collateral token backed by a regulated reinsurance pool in Bermuda. So, it’s not a traditional stablecoin pegged at $1, but rather a dollar-denominated token that appreciates over time as yields accrue to token holders.

Those yields come from the upfront premiums that insurers globally pay of the reinsurance they purchase. Those premiums, in turn, are calculated via actuarial models, meaning the yield isn’t connected to traditional crypto token volatility. They also provide ONyc with sustainable, institutional-grade returns.

By simply holding ONyc in your browser wallet, you collect your 13.5% return. The rewards do not show up as additional ONyc tokens in your account. Rather it shows up as an escalating price for each token you own. So if you have, say, $1,000 worth of ONyc, and you’re earning 13.5% per year, you will have $1,135 at the end of a year.

How to Put Money to Work With OnRe/ONyc

Once you have USDC on your browser wallet, connect to the onre.finance website. There, you will see the Deposit dialog box.

Select how much USDC you want to deposit, and you will see how much ONyc you will receive. Similar to Perena, this is not strictly a 1:1 transfer, given that ONyc’s price reflects accrued yields from the premiums collected.

You will see the yellow Purchase button. Click on that and your USDC will convert into ONyc that shows up in your browser wallet. There’s nothing else you need to do; your ONyc starts working for you immediately.

A Third Potential Airdrop Windfall

Like Perena and Loopscale, OnRe is also running a points system based on the amount of ONyc you own, and any DeFi strategies you pursue with your ONyc tokens (I’ll share one of those in a moment).

As with Loopscale, there’s talk that the ONRE token, when it drops, will give owners a share of the revenue the underlying reinsurance business generates. Again, though, I will reiterate that nothing is set in stone at this point.

Still, I own ONyc and I am looping it for additional points. And speaking of looping…

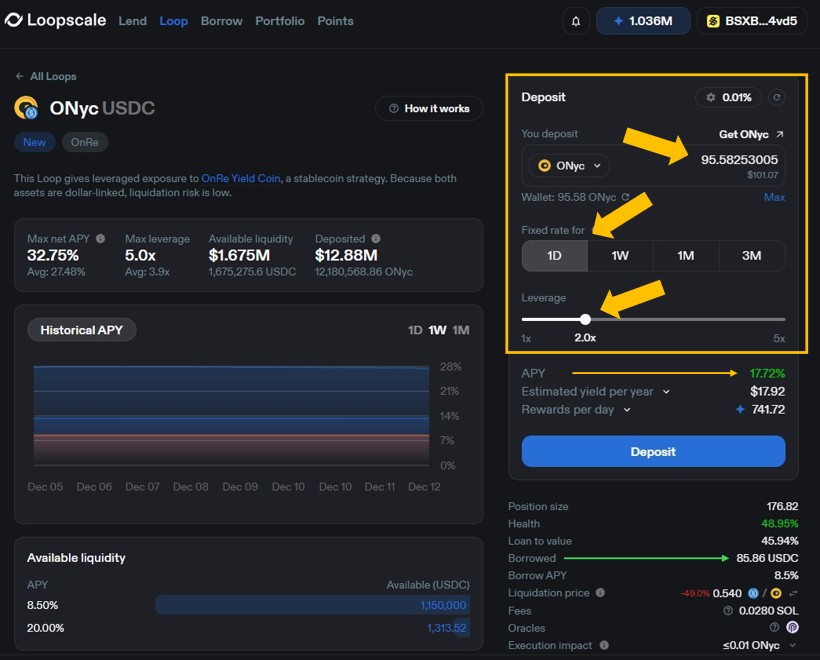

Earning More on Your ONyc by Looping It Through Loopscale

Looping is a leveraged strategy aimed at amplifying yields.

The process involves repeatedly borrowing and redepositing the same asset to amplify the yield—a strategy unlike anything you will find in the real world of banking and personal finance.

As part of the strategy, you’re supplying ONyc to your Loopscale account, and you select a leverage ratio between the 1x and 5x they’re comfortable with. Loopscale’s smart contract borrows USDC that’s used to buy more ONyc, which is then used to borrow more USDC and on and on, up to your leverage limit. (Note: Loopscale offers looping on other crypto assets as well, including USDC and Solana.)

You also have to pick a desired timeframe for the strategy—1 day, 1 week, 1 month, 3 months. Think of it no differently than choosing a time period for a certificate of deposit. I chose 1 day for the flexibility and then let the protocol auto-refinance my position for me daily.

Like I said, looping is not something you find in the real world, so let me walk you through this step by step:

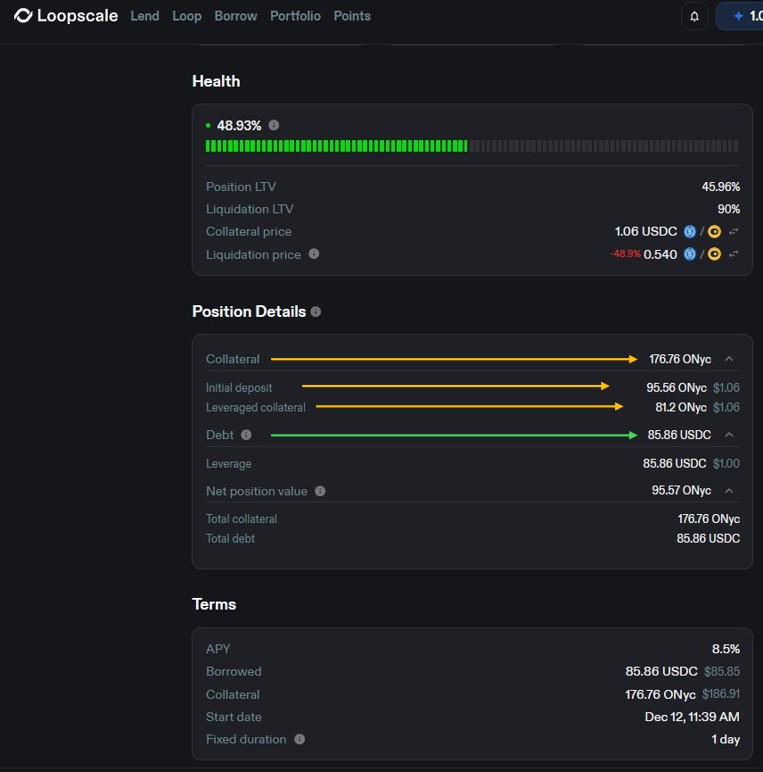

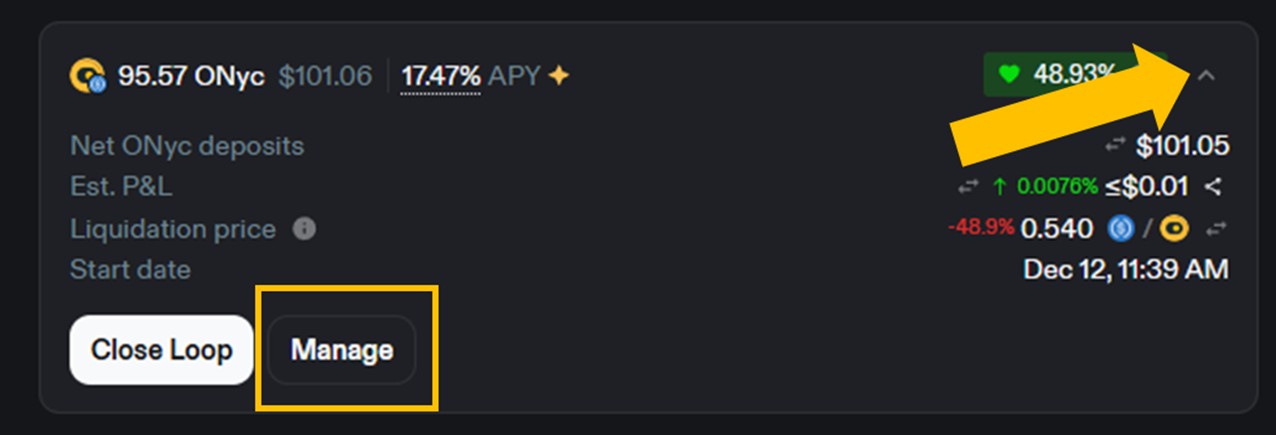

In this example, we’re going to deposit 95.5825 ONyc. (That was the amount of ONyc I received for depositing 100 USDC for this example.) Here, we’re going to select the “1D” option for a one-day cycle, and we’re using leverage of 2%. Based on those parameters, we’re collecting a yield of 17.72% at the moment, though that will go up or down. The higher the leverage, the higher the risk you take, which is why I generally stick to 2 to 2.5x leverage.

Click Deposit… and your ONyc is now working even harder for you.

Note: To reach this page, click on the “Portfolio” tab at the top of the page, and then under your Loops position, click on the down area to the far fight and then click on “Manage.”

In this strategy, you’re amplifying that original 13.5% reinsurance yield you collect on ONyc.

When you deposit your ONyc to Loopscale, the tokens leave your wallet and land in the Loopscale contract. So Loopscale is technically now earning the 13.5%.

But it’s actually earning more because the entire leveraged position is earning that yield. So your initial deposit of 95.56 ONyc is acting like a deposit of 177 ONyc. You have lending costs in the mix that you’re repaying, but your overall yield is sharply higher than if you just held ONyc in your browser wallet.

At the moment, the average yield on an ONyc looping position is about 27.9%, depending on borrowing rates, the leverage you use, and the period of time you select.

And though all of those steps in the looping process seem complicated, the entire process is automated through smart contracts, and they execute in seconds.

The Risk With Looping

Beyond a catastrophic hack, risks include liquidation if ONyc depegs (a low-risk possibility), and the risk that rising borrow costs erode your net yield.

Airdrop Bonus

By owning ONyc you are already collecting points toward a potential airdrop. But by using the looping strategy at Loopscale, you’re multiplying your daily points by 6x, which will help you to collect more ONRE tokens if an airdrop happens.

If nothing else, I hope this issue of Frontier Fortunes underscores a comment I make all the time about the ways that crypto and the blockchain are creating an entirely new basket of innovative opportunities for investors and savers to earn income from their money.

Though these strategies above are not 100% risk free, the risks are quite small. And because you’re basically working with dollar-based stablecoins, you’re not going to see the wild volatility of bitcoin, Solana, and the others.

You’re not going to shoot the lights out like you might with bitcoin and Solana, but you’re not risking the crazy downdrafts that happen. You’re just comfortably collecting double-digit yields on cash… far better than you’ll find sticking dollars in a bank account.

As we wrap up 2025, I also want to give you an update on our Energy and Metals Portfolio.

This past year has been fantastic for metals.

Gold was in an uptrend almost the entire year, and closed 2025 with a gain of roughly 65%.

Silver had an even better year—up more than 122%.

Copper, meanwhile, had a particularly bouncy year, but has ended with a gain of more than 35%.

All which means our Energy and Metals Portfolio has given us big profits.

Taseko Mines, our tiny player in copper, is now up 270%. We closed half that position over the summer with a 105% gain.

Copper, I believe, is going to see a blockbuster 2026. A supply-demand imbalance is taking shape because of operational challenges at critically important mines around the world… new projects that have been approved are not producing enough new copper to cover the supply deficit… and there are growing worries that Trump’s tariffs on copper—which hit in 2027—will cause even greater problems.

So, we’re going into a year that should be highly enriching for Taseko stockholders.

Orla Mining, our junior gold miner, is up nearly 225%. We took profits of 173% over the summer on half that position as well. Orla, which we added to the portfolio in 2023, has played out exactly as we’d hoped. The miner was just about to launch its first mine when we moved into the shares.

Today, it’s a profitable miner producing about 270,000 ounces of gold annually, and just this month the company announced its inaugural dividend payment: $0.015, payable on Feb. 10, 2026. It’s not a ton of money, but we’re now getting paid to own what was a junior miner and which has progressed into the ranks of a mid-tier miner.

My bet: Orla gets snapped up by a larger player. The buyer would grab a base of high-quality gold reserves already in production without the hassles of dealing with government permitting and building a new mine.

Keeping with smaller gold players for a beat longer…

In June, we jumped into McEwen Mining and Metalla Royalty & Streaming. Both are now up than 100% just six months later.

McEwen is our mid-tier miner started by Rob McEwen, who founded mining giant Goldcorp that Newmont, the world’s largest gold company, bought for $10 billion several years ago. McEwen is up 117% at the moment, and I see no stopping that train.

Gold prices are destined to go higher, and copper is set for a strong 2026. McEwen owns a large stake in McEwen Copper, which has a world-class copper mine in Argentina.

Metalla is our streaming company. It does nothing but invest in individual mines, and then collect a portion of the gold or the profits that “stream” forth from that mine. With gold prices rising, the value of the gold Metalla has rights to is dumping fatter profits into the company’s coffers. As noted with McEwen, that’s not going to change any time soon. Metalla is up 125%.

As we do with most positions that reach gains of triple digits, I am recommending you sell half your position in both McEwen and Metalla. In doing so, you will recoup all of your original cost, plus a bit more… and the other half of each position will continue to grow and benefit from gold’s tailwinds. It’s just that now we’re playing on house money and we do not risk any capital losses on our original investment.

Now, let’s move on to silver and our position a small miner called Silvercorp.

Silver has recently hit all-time highs above $60 per ounce, and Silvercorp has ridden that wave higher. We’re up 200% on that position at the moment.

Higher silver prices are in the offing. As I told Field Notes readers in a recent dispatch, silver historically follows what I call the “Silver Seven Step”—a seven-step process that ultimately takes silver to highs that are massively above recent lows.

This Seven Step doesn’t happen all the time. It’s usually tied to super-bull cycles in silver, and we are in one of those now. The last two times the Silver Seven Step played out, silver prices ran up 2,600% (the 1970s to 1980) and 1,100% (2000 to 2011).

Now we’re inside the next seven-step phase and I suspect silver will ultimately see prices between $100 and $300. (If I’m pressed to pick a hard number: Silver sees at least $175.)

Thus, Silvercorp should keep on keeping on with its current upward trajectory.

Still, I want to sell out of half our position to lock in a massive gain that means we will recoup our initial investment, plus an additional 50% in profits. We will allow the other half to keep working for us.

Finally, our two energy positions: Pembina Pipeline and Woodside Energy.

They’re both up as well, just not as robustly as our metals positions.

Pembina is up nearly 43%. Almost all of that is the dividend stream. We’ve collected $6.76 in dividend payments, which is precisely why I originally added Pembina to the portfolio. The majority of the Energy and Metals portfolio is riskier plays… Pembina is the steady hand send us consistent and growing dividend checks.

In the world we’re moving into—lower interest rates in the US, paired with sticky inflation—we want strong and stable dividends, and Pembina is a great play on that because its business is the boring, staid, and entirely necessary process of moving oil and gas and energy liquids through pipelines.

When boring means consistent income, boring is super-sexy.

As for Woodside Energy, it is our Australia-based oil and gas producer that is building a new liquified natural gas plant in south Louisiana that will ramp up America’s ability to ship its abundant natural gas all over the world.

We’ve only been in this stock since October, so I have nothing much to add that wasn’t already included in that issue of Frontier Fortunes. It’s up about 8% since then.

I will add that 2026 is looking good and Wall Street analysts keep nudging price targets higher.

Plus, we’re picking up another plump dividend of around 7%, which provides underlying support for the share price.

And with that, we come to the end of Frontier Fortunes—the 2025 edition. I look forward to bringing you new and interesting opportunities where I find them next year.

In the meantime, have a great holiday season.

Talk to you next quarter…

Jeff D. Opdyke

Editor, Frontier Fortunes

© Copyright 2025. All rights reserved. No part of this report may be reproduced by any means without the express written consent of the publisher. This report presents information and research believed to be reliable, but its accuracy cannot be guaranteed. There may be dangers associated with international travel and investment, and readers should investigate any opportunity fully before committing to it. Nothing in this e-newsletter should be considered personalized advice, and no communication by our employees to you should be deemed as personalized financial or investment advice, or personalized advice of any kind. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before our subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after on-line publication prior to following an initial recommendation. Any investments recommended in this letter should be made only after consulting with your investment adviser and only after reviewing the prospectus or financial statements of the company.