It’s Time to Add More Big-Potential Stocks to Our “Energy and Metals” Portfolio

Dear Frontier Fortunes Subscriber,

Typically, I launch into these cover stories by recounting a relevant anecdote. Not this time.

We’re so deep into uncharted territory that no relevant anecdotes come to mind. Well, actually, one does. But the analogy to 1930s Germany is so unsavory that some might take offense.

The reality playing out globally is that the world is on tenterhooks, uncertain of tomorrow because of a mercurial, tempestuous, and indecisive US presidential administration. The administration threatens global financial instability in the pursuit of a misguided economic agenda based on a flawed understanding of tariffs, a flawed understanding of global manufacturing processes, and a flawed understanding of government’s role in the economy.

What the world sees right now is an America that is back-sliding toward… well, no one’s sure, actually. And that’s precisely the problem.

Uncertainty is to the financial markets what sunlight is to a vampire: something to avoid at any cost.

Which is why we’re seeing so much volatility in financial markets so far this year. So much angst. It’s the entire reason the US dollar has been in retreat for almost all of 2025.

That’s the story for this quarter’s issue for Frontier Fortunes—the dollar’s decline, global uncertainty, and the impacts and opportunities we have right now in the gold and oil markets as we prepare for what’s to come.

The buck has lost more than 10% this year, not an insignificant slump in terms of currency markets.

The dollar has fallen more than 10% against a basket of currencies this year (the red box).

The US Treasury Department is struggling so mightily to auction off new US debt that it is having to pay noticeably higher interest rates to attract buyers who show up for lightly attended auctions, a situation I’ve been telling Field Notes readers was certain to arise.

And concerns are mounting that America’s fiscal situation is increasingly dire as deficits grow larger and as Congress and the White House push a bill—the so-called “Big Beautiful Bill”—that independent analysis shows would increase America’s current debt load by 10% to 15%.

These are not temporary problems.

They are problems that percolate in the minds of investors all over the world.

They are problems that, in the span of just a few months, have changed the world’s perception of America and the dollar as safe havens.

The world losing faith in Uncle Sam and his money puts at risk the dollar’s role as global reserve currency. That’s not to imply that reserve currency status could suddenly vanish next Tuesday. But it is saying that as faith erodes, demand for dollars falters… and amid that faltering, the cost of living in America goes up, draining every American family’s purchasing power.

It means the Federal Reserve will find itself in an increasingly untenable position, caught between rising prices and the government’s increasing inability to take on the annual payment obligations that arise when extreme debts run face-first into higher and higher interest rates that will be necessary to quell inflation in the economy.

In short: Crisis.

The kind of crisis that destabilizes a currency and which, in historical examples, forces governments to sharply devalue the nation’s money. Once that begins, it’s just a hop, skip, and a spit to hyperinflation.

To be clear, I am not telling you with 100% certainty that hyperinflation is in the cards. What I’m saying is that crisis is clearly brewing. That America doesn’t have an easy out at this point, and the outs that America does have will demand a painful sacrifice from the population that must suffer inflationary surges and (likely) austerity.

What I’m saying is that America faces a moment we haven’t seen in more than a century, and that our role at this point is to prepare for the risks ahead. To protect ourselves, our families, and our financial future from the very real possibility that we are moving into a new financial era in which the dollar and America are increasingly less important to the world.

In that shift, huge losses—and huge gains—are in the cards.

And, so, this issue of Frontier Fortunes is focused on helping you prepare for that risk. We’re revisiting our Energy and Metals Portfolio and prepping ourselves to profit from what’s to come.

In short, this is the case I’ll lay out for you in this issue:

Before we get too deep into this, let’s step back and look at why the world is so concerned about America today.

Please note that I’m coming at this from the perspective of an American who has lived outside of America since 2018, and who travels globally for my job. I talk to a lot of people on the road—from local business leaders and investors to local hotel clerks and taxi drivers and waitresses. What I share is what I’m told, based on how people outside of America see America changing. It’s a view a lot of Americans don’t see or don’t want to accept, but that doesn’t really matter because how people see America today defines how they interact with America.

Political polarization: The world looks at the Red/Blue divide and shakes its head at how far America has regressed toward its Civil War past. The polarization underscores perceptions that America’s political processes are broken, and that cross-aisle hatreds are going to lead to a political, social, and fiscal crisis that upends the global economy.

Economic anxiety: Despite overly massaged government data, inflation in America remains problematic. I see it for myself when traveling to the US. While prices aren’t rising as fast, they’re still rising, and they’re rising from a base that reset permanently higher in the wake of the COVID inflationary period. Today, American consumers as a group carry rising credit card balances (an indication that they’re living day-to-day on credit cards), but they’re also struggling more because delinquency rates are back to 2012 levels, i.e. levels caused by the Great Recession.

Foreign policy skepticism: Global polls show favorability toward America is in decline and that fewer and fewer people trust the US administration’s policies or its intentions. They rightly worry that the administration will unilaterally welch on treaties and agreements. As I was writing this, news emerged in the Japanese press about Japanese negotiators lamenting the impossibility of negotiating a trade deal with the Trump administration. That’s because Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick are often arguing and disagreeing amongst themselves about what the US really wants.

Trump’s Indecisiveness: The world largely sees Trump as irresolute, contradictory, and wavering, a character profile perhaps best summed up by a Financial Times columnist who coined the term “TACO trade” (Trump Always Chickens Out) to explain why stocks so frequently plunge on new tariffs Trump imposes, then rebound the minute Trump inevitably backs off. As Christopher Thornberg, founding partner at Beacon Economics in Los Angeles, told the Wall Street Journal in early June, “Where this goes all depends on what Trump decides to do next, and candidly, even Trump doesn’t know what Trump will do next.”

Debt and the Big Beautiful Bill: At $37 trillion, America’s debt is excessive and global bond investors are backing away to protect themselves. They’re worried that the US will reach a point where it cannot repay its debt and will impose some kind of fix that results in a default. Indeed, the Trump administration has already floated ideas ranging from imposing a user fee on foreign holders of US debt, to forcing foreign holders to convert existing US bonds into “zero-coupon century bonds” that offer no payment for the next 100 years, when they would finally come due.

Such fixes would see bond prices plunge and interest rates in America soar, which would create hellacious knock-on effects. Moreover, they’re losing confidence in America’s fiscal prudence. Trump’s Big Beautiful Bill would add $4 trillion to America’s debt.

To underscore America’s decaying financial situation, Moody’s, the global bond-rating agency, downgraded US debt in May. For the first time ever, all three major bond-rating agencies now have the US below top-tier status, a reality that means the US must pay even higher interest rates to attract bonds investors.

And all of this highlights why it is that the US dollar is in retreat.

The global army of investors no longer sees America as a rock of stability but as a morass of instability.

It’s the reason why gold prices are hitting record highs seemingly every other week… and why oil prices are plunging, which is setting up a rebound that will slam consumers but create huge wealth for those who own oil investments.

Let’s start with oil…

I will tell you up front that—while I’m alerting you to what’s coming down the tracks for oil—I am not going to recommend any oil stocks… at least not yet.

I will, however, be recommending oil stocks in an alert I send you later this summer.

Here’s why I’m doing it that way:

The oil market right now is in an unsettling moment because of fears about where the global economy goes as Trump’s disjointed tariff agenda plays out, and as OPEC uses this moment to try to destroy the US oil industry, particularly the companies that are producing America’s shale oil.

I will explain that paragraph in a moment.

What the unsettling moment means is that there is still, potentially, meaningful downside to oils stocks and I don’t want to step in to try to catch a falling knife.

However, the unsettling moment also means that a rebound is coming. And that rebound is going to send oil stocks sharply higher. So we want to own them, and I will explain why we want to own them. But first we have to let the unsettling moment play out.

As I was writing this, Israel attacked Iran—and that has led to s spike in oil prices. But whether the spike is temporary or not remains to be seen. Prices can jump with an exogenous event like Israel’s attack. But we want to watch for a longer-term uptrend.

Oil has been in the doldrums for a while. But, as I’ve said, that just means a sustained period of higher prices is coming soon—whatever happens between Israel and Iran.

Why has oil been in the doldrums?

Tariffs targeted at certain industries and certain countries for very specific reasons can make a lot of sense. Imposing them willy-nilly across all countries makes little sense because it doesn’t take into account so many relevant factors.

I’ll share one “for instance” to make the point: Vietnam.

Trump has imposed tariffs based on a simplistic mathematical model that basically relates US trade with a given country to how much that country buys from the US. As per that formula, the Trump administration came up with a 46% tariff on Vietnam.

But’s a bogus way to consider trade and tariffs.

The US buys a large amount of necessary goods from Vietnam—products that American consumers demand. Clothes, shoes, rice, natural rubber, tuna, and on and on. These are largely low-cost products that Americans demand because the American consumer can afford those products.

The US, however, is a country of high production. Vietnam is country of low wages; the average annual salary is just over $8,100. In the US it’s about $66,000. Vietnam buys what it can afford from the US, particularly agricultural products such as wheat, cotton, and soybean, plus certain electronic products such as iPhones, as well as machinery and chemicals.

But Vietnam will never have a trade deficit with the US. Trade between Vietnam and the US will never be balanced. The US has 300 million consumers. Vietnam has 100 million—earning on average 8x less than an American. There’s no way such numerical disparity balances out.

Similar scenarios play out all over the world, but the administration doesn’t seem to recognize this reality. So it imposes blanket tariffs that are, in turn, disrupting global trade and leading to increasing worries about a global recession.

Recessions beget falling demand for oil, which we saw in the Great Recession of 2007-09, and again during the recession spawned from the global pandemic. Worries about falling demand for oil beget falling oil prices, which is why we’ve seen oil prices fall as much as 30% this year so far. (At a price of about $64 per barrel before the recent events in the Middle East, it’s was still down more than 20% from January highs, the definition of a bear market.)

Recent prices have the industry teetering on the edge.

The Dallas branch of the Federal Reserve surveyed oil producers earlier this year and reported that the industry needs oil at about $65 to drill profitably. Below that and exploration stops. Production halts at rigs that require higher prices. And energy exploration and production companies are retrenching.

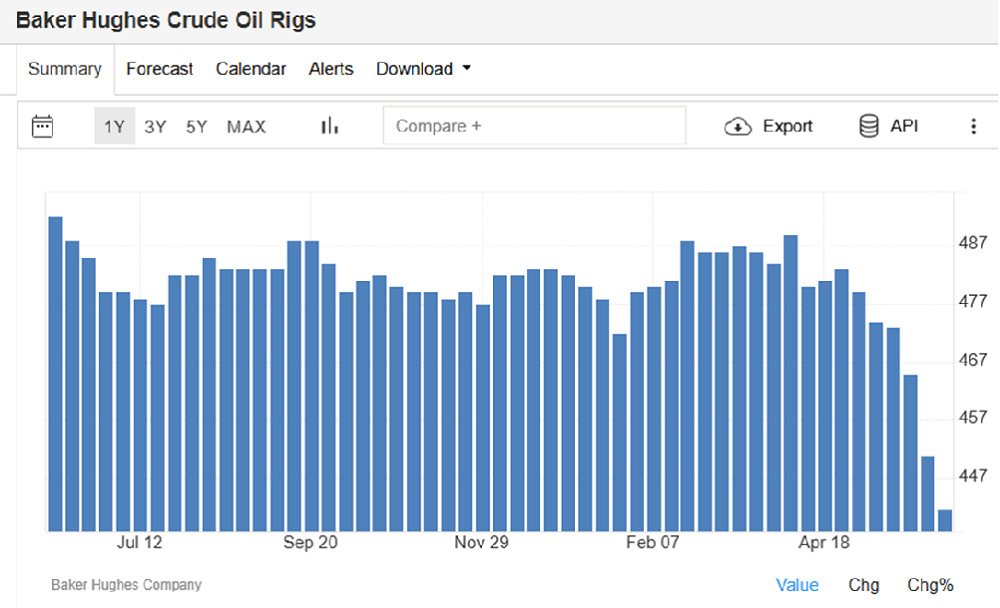

We’re already seeing that.

The number of active drilling rigs in the US has dropped noticeably from what had been a fairly steady number of active rigs over the last year. You can see the fall-off in this chart from Baker Hughes, one of the most respected providers of oilfield data. (That latest data point on the far right, though not shown on the chart, is June 6, 2025.)

As well, layoffs are roiling the industry.

Energy behemoth Chevron has announced plans to cut between 6,000 and 8,000 jobs, up to 20% of its workforce. BP and ConocoPhillips have announced big cuts, too. And there’s talk across the shale industry that producers face rough times ahead because OPEC+ has announced plans to sharply increase production.

The oil cartel increased production by 411,000 barrels in June after having increased by the same amount in May, and by 138,000 barrels in April. Expectations are that OPEC will continue these monthly increases across the summer and deep into the fall, ultimately adding more than 2.2 million barrels to the world’s daily production totals.

Such a flood of oil promises to drive prices even lower, potentially into the low $50 range, or even into the high $40s.

And that’s why I’m leery to recommend rushing into oil stocks immediately… but it’s also the reason we’re going to be rushing into oil stocks soon, and why I am writing to you about this. I want us to be prepared for the opportunity that’s coming, and I want you to understand that opportunity when I send you the buy alert later this summer.

See, oil is among the most predictably cyclical industries. It’s the most global industry on the planet because every country needs oil in some fashion to power its economy. But that also makes oil the quintessential boom/bust industry in that high prices always lead to lower prices which always lead to higher prices.

Oil in the $40 to $50 range is going to see a great deal of US production shut-in, meaning producers will stop producing because certain wells are not cost-effective to run at such low prices. It also means exploration companies will rein in their spending on finding new oil reserves to tap.

And that’s a problem because global demand for oil keeps growing.

Even though Western economies are trying to wean themselves off fossil fuels, emerging economies don’t have the luxury of chasing pricey alternative-energy technologies. Those economies continue gulping down barrels and barrels of oil, and because they’re growing much faster than the West, their insatiable demand more than offsets the West’s declining demand.

Here’s how it plays out cyclically:

That price risk exists because oil is “priced at the margin.”

If the world needs 105 million barrels per day to meet demand, but existing production can only supply 104.999 million barrels, then the question becomes: What price is necessary to produce the next barrel of oil to meet demand?

That “next barrel” is the margin.

And if that next barrel costs $70, when oil is priced at $55, then oil prices across the entire industry begin to move higher.

But then there’s not enough oil at $70 so, the next supply comes on at $85 per barrel.

And soon enough we’re quickly back above $100, and racing toward $150 or more.

“Low oil prices always beget higher oil prices… and higher oil prices always beget high prices for oil stocks.”

That is why I want to be a buyer of oil companies when oil prices are in the tank. Low oil prices always beget higher oil prices… and higher oil prices always beget high prices for oil stocks.

I don’t want to buy yet, however, because I want to gauge the impacts of OPEC+ production increases across the summer. I want to see if OPEC+ really is going to follow through with monthly production increases of 400,000 additional barrels into the fall.

If so, then oil prices will come down and so will the price of oil shares.

If not, then oil prices are going to stabilize and begin to nudge higher, which will see oil-stock prices start to move higher.

Right now, oil stocks have come off sharply. Many are in their own bear market. One I particularly like, and which has strong ties to the liquified natural gas industry, is down 35% from 2023 highs (I’m likely to recommend you buy this one in the alert later this summer). Major oil giants like BP are down more than 20% in the last year or so.

But we’re going to wait this out a bit.

Even though prices for many oil companies represent compelling bargains (BP is so low its dividend yield is above 6%, well beyond the 3% to 4% range of the last 20 years), I suspect prices will slide further as OPEC+ lives up to its promise of adding 2.2 million barrels of production through the fall.

So we wait.

Just be prepared, though, for the trade alert to come. Because we’re going to snap up high-quality oil shares on the cheap and ride them much higher as oil prices inevitably rebound. Indeed, the conflict in the Middle East has already seen oil prices spike sharply. But it remains to be seen if that will lead to a more sustained rebound.

So, watch your email for an alert very soon.

Now, let’s move on to gold, where we do have some buying opportunities.

The first question I have to answer is one I hear regularly: Haven’t I already missed the runup in gold?

Yes and no.

Yes in that gold has risen to about $3,330 as I write this, just off the all-time high of $3,500 per ounce that it hit in April. I have been recommending gold since it was $1,000 per ounce 15 years ago. And all along the way, as gold hit $1,500, $2,000, $2,500, etc., people have asked that same question: Haven’t I already missed the runup?

Each time I said “no” because the fundamental drivers propelling gold’s price haven’t changed. In fact, those fundamental drivers have intensified.

Primarily that’s America’s egregious amount of debt; its increasingly large annual debt repayment obligations that now hit $1 trillion annually, or more than 15% of the budget; the country’s increasingly fractious and hateful political rhetoric; the very real risk that bond investors continue pushing market interest rates higher, or simply stop attending Treasury bond auctions (as they’re already doing), which will force the Treasury to pay higher interest rates on US debt (exacerbating the annual interest cost challenge); and the possibility, as the Trump administration has hinted at, that the US will impose some form of capital controls on foreign investors, which would create pandemonium in the financial markets.

Topping all of that is the sad reality that foreign investors, as I pointed out earlier in this issue, are increasingly stepping away from the US. They’re selling out of American stocks, US debt, and the dollar, and they’re taking that cash back home.

That weakens the US financial system and, more worrisome, creates an environment in which interest rates keep rising, leading to a monetary melt down.

To be clear, I’m not talking about the interest rates the Federal Reserve sets. I’m talking about the interest rates the market sets when it bids on US Treasury bonds. As demand for bonds falls off, rates have to go up so that Treasury can entice enough buyers to buy all the debt the Treasury Department needs to sell. Those interest rates play through the economy. Rates on the 10-year Treasury bond, for instance, determine mortgage rates… which is why 30-year mortgage rates have pushed to about 7% today from 2.6% five years ago, tracking the increase in 10-year Treasuries that have jumped to 4.5% from just 0.6% over the last five years.

All of those risks are why gold prices keep climbing ever higher (since gold is the original safe-haven asset), and why I am convinced that gold will see $10,000 before it ever sees $1,000 again.

Which is why the other half of my answer to that question is “no”—you’re not too late to invest in gold.

There’s no indication anywhere that the US is on the path of fiscal prudence.

Just the opposite, actually.

As I noted with earlier comments about the Big Beautiful Bill, the US remains firmly committed to the path of perdition. That will never change until a crisis beyond Congress’ control forces a change. In pushing a bill that adds $4 trillion to America’s already problematic pile of debt, Republicans are erasing pretense that the GOP is the party of fiscal conservatives (statistically, that was never the case, but the GOP spin machine has done a great job of farming that fabrication).

The world recognizes this reality too, which, again, is just another reason gold remains buoyant well above $3,000 per ounce.

We’ve seen central banks all over the world load up on gold at a pace that mirrors central bank gold buying back in the 1960s, before the US was forced to abandon the gold standard.

Early on, gold miners didn’t much respond to gold prices racing higher. That’s largely because gold’s rapid ascent began as post-pandemic inflation took off, which raised miners’ operating costs for everything from salaries to energy to replacement parts for mining equipment.

That inflationary bulge moderated in 2024, and combined with continually increasing gold prices, mining stocks have started to move.

“There’s still lots of room for gold to run over the long-term.”

But there’s still lots of room to run over the long-term.

Which is why I am adding two new gold positions to the Frontier Fortunes Energy and Metals Portfolio

The first addition is a mid-tier miner, McEwen Mining.

Toronto-based McEwen mines a few different metals—gold, silver, and copper. So we get exposure to all of those. And I just happen to like all of those. Gold for all the reasons laid out above; copper because the world is re-electrifying around renewable energy, and that requires an awful lot of copper; and silver, because it’s also much-needed in the green-energy transition, as well as the fact that mine supply is tight because silver is largely a byproduct of gold and copper production.

McEwen operates three gold mines—one each in the US, Canada, and Argentina—as well as a silver mine in Argentina. It’s also developing a copper mine in western Argentina, along the Chilean border, a pocket of the Andes Mountains known for its rich ores. That development, known as Los Azules, is one of the 10 largest undeveloped copper deposits in the world. (Los Azules also holds an estimated 5.5 million ounces of gold, 191 million ounces of silver, and 251 million pounds of molybdenum, largely used in the steel industry.)

Here, I could throw out a bunch of good numbers, but honestly a bunch of good numbers is not what excites me the most about McEwen Mining. Instead I am excited by two facts:

Each McEwen Mining share represents three businesses:

Combined, those businesses are worth, roughly, between $13.50 and $47 per share, depending on whether assets are valued at their lowest or highest valuations.

McEwen Mining’s stock as I write this sells for just $9.36 per share.

As such, I see compelling upside in McEwen.

We’ve not yet really seen the retail crowd move into mining shares. The focus has largely been central bank gold buying and mom-and-pop investors snapping up one-ounce bars and coins at Costco and local coin dealers.

The move into mining stocks is now happening, but it’s early innings yet.

When the focus turns to mid-tier miners, McEwen is going to stand out, and the gap between price and the shares’ underlying value will rapidly narrow.

Though McEwen is a Canadian company, you’ll find the shares trading in New York, so they will be easy to buy through any brokerage firm.

My second recommendation is Metalla Royalty & Streaming.

Unlike McEwen, Vancouver-based Metalla doesn’t own or operate any mines. Instead, it invests in mines and collects a share of the income, or a share of the metals that each mine produces—a “stream” of metals or money. Thus, the term “streaming company” or “metals streamer.”

A royalty it owns on a mine in the Brazilian state of Pará is a great example of how Metalla operates, and the opportunity we have.

That Brazilian mine is known as Tocantinzinho, operated by G Mining Ventures (a stock I recommended to my Global Intelligence readers in January, and which is already up more than 42%). Metalla bought that royalty four years ago for $9 million.

G Mining launched production at Tocantinzinho last fall. Metalla will collect between 1,300 and 1,500 so-called “gold equivalent ounces” this year, making Tocantinzinho the company’s largest streaming asset for 2025. At current prices in the $3,300 range, those ounces mean as much as $4.9 million in revenue for Metalla, meaning a payback period of basically just two years on the company’s original investment in the Brazilian mine.

Through the end of the decade, Metalla has a string of several similar streams primed to come online. This year, for instance, the Endeavor mine will begin production in southeastern Australia, and should begin contributing to Metalla’s revenue stream in the second half of the year, and then grow into the largest stream in 2026.

In 2027, Metalla management expects Canada’s Cote mine will begin production. Management expects that royalty stream could come to define the company as Metalla’s cornerstone asset. The company paid $6 million to buy that stream four years ago, but based on the reserve expansion that has occurred at that mine, the value to Metalla could well be $200 million worth in revenue over the life of the mine.

Right now, Metalla has six royalty streams that produced roughly 2,400 ounces of gold for the company last year. This year, that number should push toward 4,000 ounces, and then 6,500 ounces in 2026.

Based on mine-development timelines, Metalla is looking at as many as 17 royalty streams producing a minimum of 15,000 ounces of gold, and potentially as much as 30,000 ounces. At the minimum, that represents production growth compounding at about 35% per year over the next four years alone.

All of which is why I want Metalla in our portfolio.

The company has a good history of identifying mispriced assets long before production begins, and then reaping the rewards as the reserve base expands. Moreover, as the price of gold continues its ascent, the increased stream of gold flowing into Metalla means a huge revenue bump. That is not yet priced into this stock.

As the market recognizes what’s going on at Metalla, and as it sees revenue ramping higher, I expect we’re going to see a very nice pop in this stock that gives us a 2x or 3x on these shares.

Again, even though this is a Canadian company, you can buy the shares on the New York Stock Exchange, so you will have no trouble placing an order on any US brokerage platform. As I write this, Metalla shares are trading at $3.63.

I’ve given McEwen shares a higher risk rating because this is a mining company, and they are rich with risks, everything from geopolitical risk, jurisdictional risk, corporate risk, mining risk, economic, and more.

So if you cannot stomach a lot of risk and the possibility that these shares sink for whatever reason, then I would steer clear of them and just own physical gold.

I’m giving Metalla the same risk profile as I gave to McEwen, for the same reasons.

At the end of the day, gold has not yet seen its ultimate high price. Yes, it has consistently marched higher and higher over the last 20 years, but that march will continue because America’s fiscal challenges are worsening by the day, and there is no legitimate effort anywhere inside of government to address the profligacy. A crisis is all but assured at this point.

And if nothing else, the dollar’s purchasing power will continue to erode relative to gold, which means gold’s price continues to rise simply because the dollar is less and less.

“With McEwen, we could be looking at a 4x or more price run-up.”

McEwen and Metalla will serve us well as that trend continues unabated.

For Metalla, my immediate price projection is $7. Longer-term I think this stock hits $10, doubling from where we are now. Price. Ultimately, I think we see new all-time highs above $13.50.

With McEwen, $16 is my short-term projection. Longer-term we could again see highs near $50, after a pause in the $22 to $25 range. So we could be looking at a 4x or more price run-up here.

As I sat down to write this portfolio review, Israel has launched rockets against Iran. So, yet again, the world’s financial markets find themselves beholden to actions in the Middle East.

Twitter/X is all atwitter with chatter about World War III.

That assessment seems a bridge too far to me.

But stocks and crypto are certainly reacting to the worriers. I woke up to find my phone’s lock-screen filled with alerts about this crypto being down 9%, this other down 12%.

It’s… frustrating,

Not the losses; they’ll bounce back.

Frustrating that our world has devolved so markedly in the last 30 years...

But I will leave geopolitics there for now!

I’ve been threatening for months now to tell you about “AI Agents” and decentralized science, or DeSci, as it’s called.

So I figured now is a good time to tell you more about those areas of crypto.

We own exposure through SkAInet (AI agents) and Cerebrum DAO (DeSci). Both are deeply underwater and I want to address that.

First, a bit about each sector:

AI Agents

Simply, these agents are autonomous software systems that can act and react on their own to whatever prompts and inputs they’re given. At a very simple level, Siri is an AI Agent. You say, “Hey, Siri, where’s the nearest Starbucks?” and based on your phone’s GPS coordinates, Siri is able scan known Starbucks locations near you (blindingly fast) and pinpoint the one closest to you, and then dish up the direction.

Again, that’s a very simplistic version of AI Agents. They will become so powerful before the end of this decade that they will emerge as digital butlers that all of us have access to in the palm of our hand or on laptop and desktop computers.

They’re already in use as customer service agents; they’re working in e-commerce to optimize inventory management and to provide customers with personalized product recommendations; they’re at work inside autonomous vehicles and they’re optimizing transportation routes and managing traffic flow; financial service companies have deployed them to detect fraud, assess risk, automate trade, and to create personalized financial advice and manage portfolios.

I could keep going, but you get the point.

This is all first-iteration stuff, like the earliest days of the internet, when we were all agog over MapQuest, Ask Jeeves, and the Mozilla Firefox browser.

And look where we are today… talking about AI Agents.

Agents will be everywhere in the future. Some will be generalists, helping with pretty much everything, but at a cursory level. Others will be specialists, programmed with highly specific knowledge to manage highly specific tasks. And still others will be shepherds overseeing a flock of specialist agents and corralling them for their owners.

The one we own, SkAInet, aims to be a marketplace of agents, where agent builders can list their agents for sale or lease, and where people who don’t have developer/programmer skills can go shop for the kinds of agents they need for generic and specialized tasks. It’s a great idea, and one with obviously foreseeable demand.

The problem is that the lead developer for SkAInet has stepped away temporarily to deal with family matters. And the market has moved on. That’s the way it is in crypto, where attention spans are shorter than a mayfly’s life cycle (less than two days, and generally just one).

Moreover, while the company is still building, it’s not pushing any product at the moment because the crypto market has been in such a manic-depressive state since Trump’s election. (That’s not a Trump comment; it’s a crypto-bro comment. Crypto bros have been cycling through mania and depression since Trump’s win, emboldened by Trump’s pro-crypto stance, only to be kneecapped by the on/off tariff craziness.)

I’m patiently holding SkAInet and allowing the lead dev to deal with family matters. I will give the company the benefit of the doubt because I’ve been in crypto since 2017 and I have lived the manic-depressive phases several times. I know that once mania takes flight, crypto prices can move with lightning speed.

So, we wait…

Decentralized Science

DeSci uses blockchain technology to decentralize scientific research—meaning to make scientific research more open, accessible, and collaborative. The aim is to democratize science by providing alternative funding mechanisms, open access to data, and incentivizing researchers to share their work. In doing so, DeSci reduces barriers to entry, enhances transparency, and improves the reproducibility of research.

We’re currently in an environment where DeSci has a bright future—for the wrong reason.

Science in America has suffered severe cuts in government funding this year. And that means a decentralized approach to science may be increasingly important to human health, because Uncle Sam is no longer backing up science in the same way.

Among the many DeSci projects underway at the moment are one focused on longevity research and regenerative medicine; women's health research in areas such as endometriosis, which may be underfunded by traditional means; hair restoration treatments; critical environmental projects; and others.

Our DeSci play, Cerebrum DAO, focuses its efforts on brain health and neurodegenerative diseases. The company’s crypto token, NEURON, gives holders discounted access to brain health products, and early access to therapeutics, among other benefits.

The project grew out of the founder’s own life. His youngest daughter has Down syndrome, which makes her more susceptible to early onset dementia and Alzheimer's. She needs therapeutics to help stave that off, yet despite all the money thrown at Alzheimer’s, the medical industry has little to show for that effort.

So Cerebrum DAO was born out of frustration with the existing medical-research infrastructure.

The tokens are down markedly, but again that’s a function of crypto bros and their “squirrel!” syndrome. They quickly flit from one sector to another, and then to another. But what I care about as an investor in crypto is: Is the company progressing?

And Cerebrum is progressing. It has been active in DeSci conferences across the cryptosphere and across the globe, and has:

I can’t promise all of that leads to a moonshot crypto at some point. But they are milestones that give me compelling reasons to continue to hold onto Cerebrum DAO as the DeSci trend gains traction.

So, that’s where we stand with these two emerging, exciting crypto sectors and my picks for each.

As so often when it comes to crypto... Patience is the name of the game.

Talk to you next quarter…

Jeff D. Opdyke

Editor, Frontier Fortunes

© Copyright 2025. All rights reserved. No part of this report may be reproduced by any means without the express written consent of the publisher. This report presents information and research believed to be reliable, but its accuracy cannot be guaranteed. There may be dangers associated with international travel and investment, and readers should investigate any opportunity fully before committing to it. Nothing in this e-newsletter should be considered personalized advice, and no communication by our employees to you should be deemed as personalized financial or investment advice, or personalized advice of any kind. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before our subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after on-line publication prior to following an initial recommendation. Any investments recommended in this letter should be made only after consulting with your investment adviser and only after reviewing the prospectus or financial statements of the company.