Dear Global Intelligence Letter subscriber,

He was known as The Silver King.

The stone-cutter who became one of the richest and most successful silver mining magnates in Colorado.

But Horace Tabor had not come looking for silver, he had come—like so many others—in search of gold.

It was 1859, four years after the California Gold Rush had ended. Prospectors were desperate for new rivers to pan and new veins to mine. Then word began circulating: Gold had been found in the eastern Rockies, in a place called Pikes Peak County, near present-day Denver.

The Colorado Gold Rush was on.

Over the next few years, some 100,000 gold seekers descended on the region to find their fortune. They were called the Fifty-Niners, for the year in which most arrived. Their motto was “Pikes Peak or Bust!”

Among these Fifty-Niners was former stone-cutter Horace and his wife, Augusta. While he sought gold, she ran a store. Their storekeeping was a success, but their prospecting was not, and by the mid-1860s, the gold had dried up without Horace making his fortune.

His luck, however, would change utterly a decade or so later.

In the late 1870s, Horace, then still a shopkeeper, agreed to provision two prospectors in exchange for one-third of their discovery.

The two men, August Rische and George Hook, found massive silver lodes. And, they did so just as Congress authorized large-scale purchases of silver under the Bland-Allison Act. This law required the Treasury to buy a certain amount of silver and put it into circulation as silver dollars.

Demand for silver exploded, sparking the Colorado Silver Boom.

Horace became super rich. He established newspapers and a bank, built opera houses, and served as a senator and lieutenant governor of Colorado. He was even mired in a famous scandal, when he divorced Augusta, his wife of 25 years, to marry a woman half his age.

But Horace was as adept at squandering his money as investing it. When the government reversed its silver-buying policies in 1893, he lost everything.

So it goes with silver. The metal is often viewed merely as gold’s sidekick, the Robin to gold’s Batman. But it has unique qualities. Prices tend to be more erratic, more volatile. Traders call it the devil’s metal.

However, history has shown time and again that if you catch silver at just the right moment, at the point of an upswing, it will reward you with truly astonishing gains.

We are on the verge of just such a moment—a new silver boom.

This time, the reason is not a government silver-buying program. It’s a confluence of factors that are now emerging to push silver higher.

One factor behind silver’s impending rise is the commodity super-cycle I wrote about in last month’s issue. Silver will benefit in a big way from that trend, as demand for the metal is growing.

Another factor is a major rule change, whose effects will spread across the world’s precious-metal markets over the next six months. This will fundamentally alter how gold and silver are traded.

Once the full impact of these events is felt, silver will rocket in the years ahead—to never-before-seen highs.

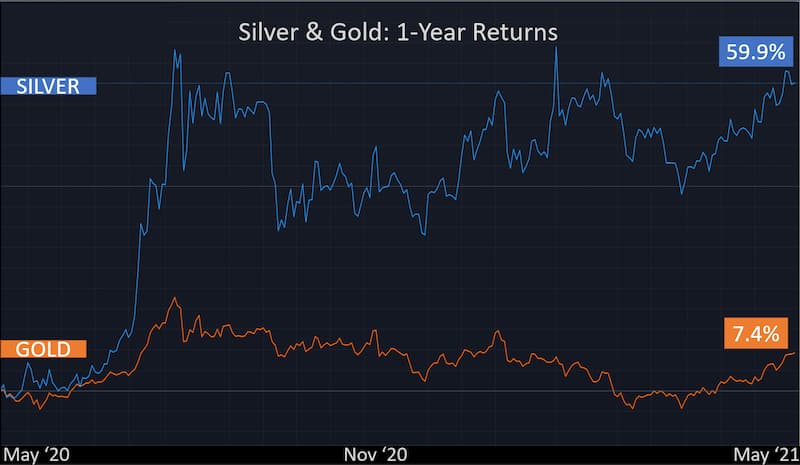

Silver is a hot commodity these days.

The Silver Institute, an industry trade group, projects demand this year will jump 11%. This is largely thanks to a global economic rebound as the post-pandemic world reopens.

You see, unlike gold, silver is a commodity that is consumed as well as stored. It’s an industrial metal used in electric vehicles, solar panels, and 5G telecom. So, silver is right in the wheelhouse of some of the hottest industries on the planet these days.

That means it is very much in demand right now, amid the commodity super-cycle I wrote about in the May issue.

You can see that in this chart of gold and silver prices over the past year…

However, this spike in demand for silver is running headlong into falling supply.

Earlier this year, the U.S. Geological Survey published a report on global silver production and global silver reserves.

Both are heading south.

See, silver is largely a byproduct metal, not a primary metal. By that, I mean silver is produced almost as an afterthought from copper, gold, lead, and zinc mining.

This means most silver-mining companies nowadays aren’t specifically hunting for silver. But they’re happy enough to produce silver when they come across it in their primary mining efforts.

The 10 largest silver-producing countries represent a combined 86% of global, annual silver production.

Almost all of them have seen a decline in output over the last five or six years.

Some of that is the impact of the pandemic that shuttered a host of mining operations. But for most of these countries, COVID only worsened a trend that was already underway.

When rising demand meets falling supply, prices move in one direction: up.

But silver also has a “technical tailwind” that could see the price shoot even higher.

Here’s what I mean…

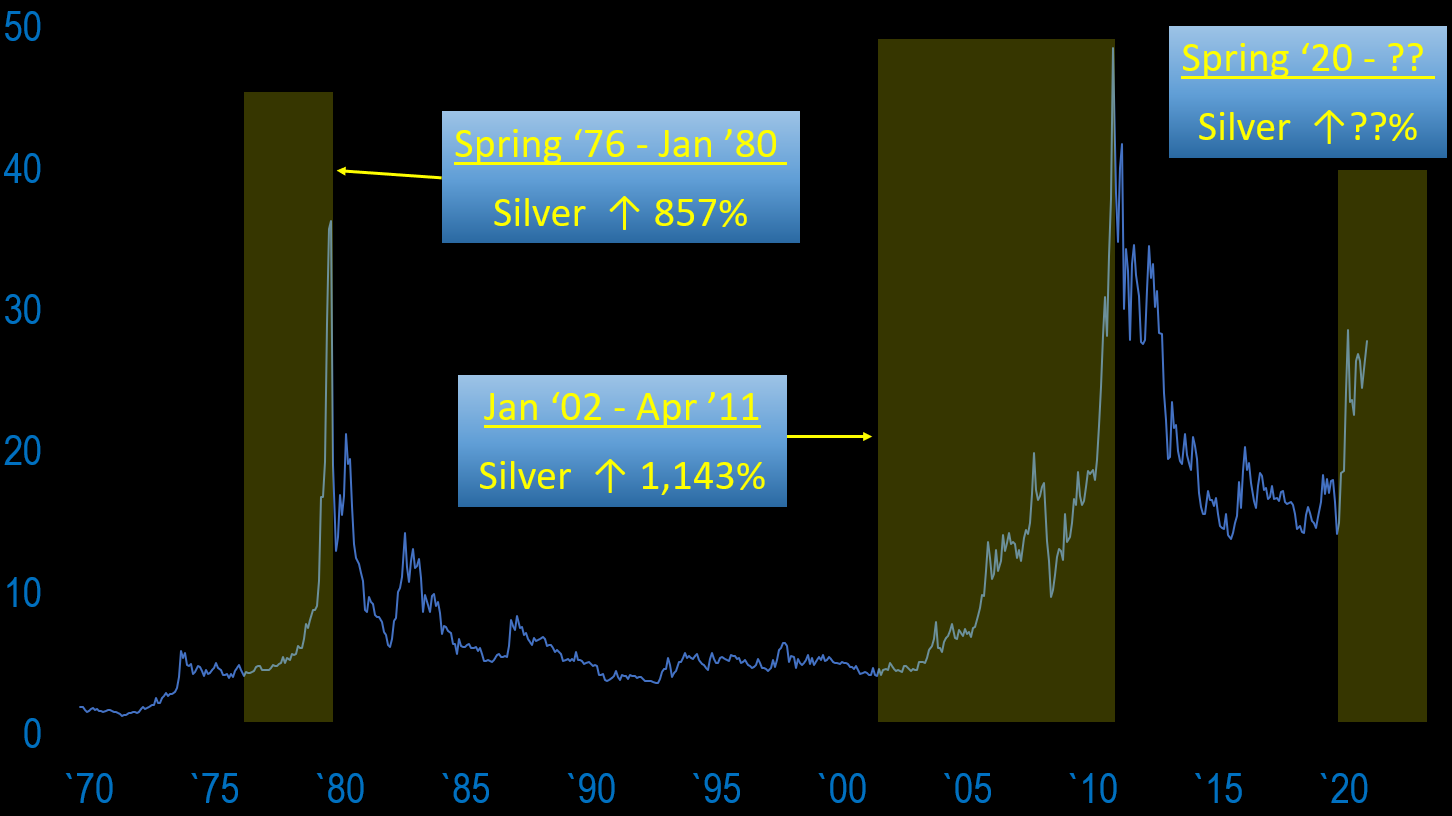

Twice in the past 45 years, silver prices have achieved massive, multi-hundred percent gains. From the mid-1970s through January 1980, and from the early-2000s through 2011, silver prices followed an identical path and jumped massively.

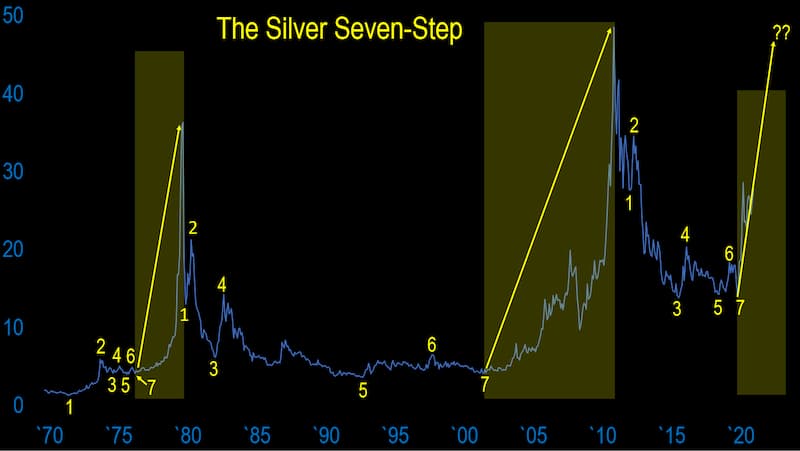

The two previous times silver exploded higher, the metal followed the same pattern, what I call the “Silver Seven-Step.”

This seven-step movement is a traditional, long-term pattern that applies to any asset, and it is almost always a bullish sign. It points to explosively higher prices.

The numbers 1 through 7 mark a progression of highs and lows that occur over longer stretches of time.

Silver last peaked in 2011 at a record high near $50 per ounce. Since then, it has spent the decade wandering a wintery wilderness, as did almost all commodities. But now, winter is over. As I wrote about last month, the summer of commodities is upon us.

In line with the seven-step pattern, silver has tried to break out on three occasions since 2011 (#2, #4, #6), and each time it failed. But March 2020 saw a change of sentiment (#7). Silver jumped due to the pandemic.

And now that every major economy on the planet is spending cash to rebuild what the pandemic destroyed, that chart of silver leads me to two truths:

Better yet for silver investors, those two truths have emerged just as a major change in the precious metals market is about to put upward pressure on silver prices. That change is tied to something called Basel III.

To understand how Basel III will lead to a spike in prices, we first need to understand how the gold and silver markets currently operate.

The largest and oldest precious metals market in the world is the London Bullion Market.

Every week, between $26 billion and $30 billion of gold and $5 billion of silver trades through this market.

The great majority of that, 90% or more, is not physical metal. It’s pieces of paper swapping hands between traders, borrowers, and lenders.

In theory, those pieces of paper represent real gold and real silver. I say “in theory” because the amount of paper gold and paper silver that trades far exceeds the world’s known supply of gold and silver. There’s no way each piece of paper is actually a claim on physical gold or silver. There’s simply not enough real metal to go around.

This is a concern to something called the Bank of International Settlements, the central bank to the world’s central bankers.

So, it’s changing the rules of the game.

To prevent banks from overextending themselves in precious metals, the Bank of International Settlements has authored a new set of rules called Basel III. These rules call for banks to have sufficient capital reserves in place to cover losses, particularly when it comes to all this paper trading in gold and silver.

Specifically, the rules will require banks to hold reserves equal to 85% of the value of the gold and silver contracts on their books.

On June 28, this rule takes effect across most of Europe.

But this will be just the precursor to the main event…when Basel III comes into effect in the U.K. in January 2022.

The London market is run by the London Bullion Market Association. And come January, members of the LBMA—which include many of the world’s largest investment banks—will be subject to Basel III rules. And they are not happy about it.

Banks profit by investing and trading money, not by storing it as reserves. By forcing them to tie up a lot of capital, Basel III will prove very costly for banks.

The LBMA has told the Bank of International Settlements, the European Banking Authority, and the Federal Reserve that it’s worried about “the damaging effect that the rules will have on the precious metals…system, potentially undermining the system completely.”

It concludes that the impact of Basel III “would be felt globally [and] would fundamentally alter” the market for gold and silver.

In short, the LBMA says that because of the costs associated with Basel III, a significant number of banks are likely to scale back their paper trading in precious metals. Some may even walk away from it entirely.

This may not sound like a positive development for the gold and silver market…until you realize that major banks have had their fingers on the scales for decades.

Here’s why a drop-off in paper trading is bullish for silver.

Assume for a moment that there exists just 1 million ounces of physical silver in the world, and that there are 2 million buyers who want to own silver. Well, those 2 million buyers establish a price for those real ounces of silver. As demand rises, silver prices rise, too.

But then along comes a bank that creates 1,000 silver contracts, each of which represents 1,000 ounces of underlying silver. This has the effect of adding another 1 million ounces of silver to the market. But while those contracts represent real silver, the bank itself doesn’t own the metal; it has borrowed it.

Nevertheless, it now looks like there are 2 million ounces of silver in the market—the 1 million physical ounces, and the 1 million paper ounces. That means the price of the metal falls because now there is apparently far more silver—more supply to meet the demand.

Now, let’s take away all those paper contracts …

Suddenly, those 2 million buyers of silver realize that there’s not really 2 million ounces of silver…there’s only 1 million real ounces. Prices move higher on reduced supply in the face of the same or growing demand.

There’s also another reason less paper trading will be good for us…

Right now, because 90% of gold and silver trading is just paper contracts, banks can manipulate precious metal prices.

That might sound like a conspiracy theory, but price suppression has been part of precious metals trading for decades, particularly in the silver market.

Just last year, JP Morgan paid a huge, $920 million fine for manipulating precious metal prices over many years. I can assure you, JP Morgan is not a lone wolf.

Here’s an example of how banks manipulate prices: A bank (or cabal of banks) will sell a huge amount of silver that it does not own. To do this, it borrows that silver from another bank and immediately sells the metal at the market price. Let’s say it sells silver at $25 per ounce.

Well, supply-demand economics tell us that selling increases the supply of an asset, and the increasing supply drives down the price.

So, by selling large sums of silver it doesn’t own, a bank can (and does) create artificial supply to drive the price down to, say, $18.

That, in turn, allows the bank to buy back and replace at $18 all the silver it borrowed and sold at $25. It gets to keep the $7 per ounce as its profit for manipulating the market. All that borrowing, however, is not physical silver. Again, it’s all paper contracts. Under Basel III, this will be difficult or even impossible.

So when paper trading is less prominent in the precious metals market, and when price manipulation is less common, gold and silver will rise in price.

That won’t happen immediately. It will take some time to work through the system. We will see an impact when Basel III comes into effect in Europe later this month, and this will grow over the next six months as London banks prepare for its arrival.

But the time to buy the assets is before this happens and the real market takes over from the suppressed, manipulated market controlled by the big banks.

I remain a big fan of gold; I expect gold, at $1,875 per ounce as I write this, will reprice above $2,100.

But, I think silver is the better buy at the moment.

Not only does it face a 30% or greater move up because of Basel III, it has the tailwinds I described above: the demand/supply issues, and the Silver Seven-Step pattern now unfolding.

Which leads to the Big Question: How high will silver climb?

Based on the Silver Seven-Step charts, it’s easy to expect that silver will rise at least 1,000% from its March 2020 low in the $14 to $15 range.

That means we’re looking at silver prices that could very well touch new record highs near $150 per ounce. Given silver’s current price in the $27 range, we’re talking about potential gains of 450% or more from where we are today.

But I think $150 might be light because we also have to consider the impact of Basel III.

As I noted earlier, by removing artificial suppression from the market, that rule change will very likely reprice silver permanently higher over the remainder of 2021 and going into 2022. I estimate silver’s new, post-Basel floor in the $35 range, or about 30% higher from its current price.

If we retroactively assume Basel III was in place last year, then silver’s $14 to $15 price in March 2020 would be more like $18.50 to $20. Meaning a 1,000% run from that level would put silver up near $200 per ounce. That’s a gain of more than 600% from the $27 price range today.

And that’s my expectation—that silver sees an epic run from around $27 per ounce today toward $200 tomorrow.

When is “tomorrow?” That’s difficult to say. But as I mentioned in the May issue, commodity super-cycles often run a decade or longer.

And as the Silver Seven-Step charts show, silver’s move from step #7 to its next all-time high occurs over a number of years. So, I will say that silver hits $200 per ounce this decade, probably by 2027.

There are numerous ways to buy silver. Exchange-traded funds; shares of silver-mining companies; silver futures contracts; pre-1964 dimes, quarters, half-dollars, and dollars that contain either 40% or 90% silver. Of these, our best option by far is owning physical silver.

Now, of course, our Global Intelligence Letter portfolio already contains a gold-related ETF, so you may be wondering why there isn’t an alternative for silver.

Our ETF is for gold miners, so it gives us a convenient way to invest in the companies that control the supply of physical gold. However, as I mentioned, a lot of silver is produced as a byproduct of other mining operations, so we don’t have a similarly good option for silver.

So, our best way to profit from the rising price of silver is to purchase the metal directly.

I’ve been adding physical metal to my portfolio for decades. My largest exposure to silver is physical silver bullion in the form of coins produced by national mints in the U.S., Canada, the U.K., Austria, and Singapore.

These are instantly recognizable, instantly tradable, one-ounce bullion coins such as the U.S. Silver Eagle, the Canadian Maple Leaf, or the Austrian Philharmonic, to name three.

They all follow the market price of silver, with a small premium attached to cover the cost of actually minting the coin.

If I wanted to sell my silver bullion, I could sell it back to the dealer I bought it from, and the transaction would be instantaneous because these coins are a known quantity and their prices are up-to-the-moment.

Though these coins are physical, I don’t physically have possession of them.

I keep them in storage, in secured vaults, with the trading companies—or even the national mints—that I do business with. And the trading company I’m recommending to you is BullionStar in Singapore. (To be clear, I earn no benefit if you trade there. I’m just sharing with you what I do and where I do it.)

BullionStar is globally renowned for its metals trading, so this isn’t some small firm on the other side of the planet. The company trades in precious metals from mints all over the world. I can conduct all of my trading online. I can conveniently get money into my account through an online transfer connected to my bank.

It offers some of the best prices I’ve found, which means the premium it charges on top of a metal’s market price is narrower than just about any dealer I’ve come across in my personal trading.

And, better yet, BullionStar offers storage services—meaning that I effectively have my very own, personal silver bullion vault. If I want delivery of my coins, BullionStar will arrange that. But I can also buy my silver and request that BullionStar hold it for me in its highly secure vaults in either Singapore or New Zealand.

As for an exit strategy, I can sell my silver and the money shows up in my account immediately, allowing me to transfer it directly back to my attached bank account.

Or—and this is what I truly appreciate—I can walk into BullionStar’s showroom in Singapore and immediately withdraw my silver from the vault and take physical possession of it. That, to me, is interesting amid a world in which I no longer trust indebted Western governments to do the right thing.

Why Singapore? Well, for a few reasons.

My recommendation, thus, is to buy one-ounce silver bullion, as much as you feel comfortable owning. You can take physical possession of your coins, if you want to store them at home or in a safe-deposit box. But if you want some of your wealth offshore, then I recommend buying and holding your bullion through BullionStar’s vault service. For silver, you will pay an annual storage fee of 0.59% of the value of the metal you own.

It doesn’t matter which kind of one-ounce bullion coin you buy, whether it’s the U.S. Silver Eagle, the Canadian Maple Leaf, or whatever. I would simply buy whatever bullion is the cheapest on the day. Silver is silver, after all.

If you feel more comfortable buying silver in the U.S. and having it shipped to your home, then I would recommend Boston Bullion. Again, I have no ties here. But I’ve kept up with this small, Massachusetts dealer since my days writing about metals for The Wall Street Journal, and Boston Bullion offers some of the lowest markups I’ve ever found. You won’t have offshore storage options, though, if you wish to pursue that.

Our portfolio continues to perform well.

In mid-May I sent out a portfolio update letting you know that we’d reached the buy limit on our position in iShares MSCI Global Gold Miners ETF. I set a limit at $32 and we’re now about $33, meaning our gold mining exposure is up around 29% since March.

This ETF has more gas in the tank, for sure, because of the era we’re now in. I’ve been writing to you recently here in the Global Intelligence Letter and my daily Field Notes about inflation and, well, inflation has arrived sooner than expected. The government reported blow-out inflation numbers recently at the consumer and producer level—numbers not seen in decades.

Treasury and Fed officials say it’s all transitory and “trust us—we got this.”

As President Reagan once said: “The nine most terrifying words in the English language are, ‘I’m from the government and I’m here to help.’”

I think the Fed and Treasury are blowing smoke to keep the masses happy, so hold onto your gold exposure for what’s about to transpire in our economy.

Our position in Norwegian krone, the currency of Norway, also continues to press methodically higher. We’re up more than 3% on that, which is nice for a move in the currency market, where 4% or 5% is a good move in a year.

The Norges Bank, Norway’s version of the Federal Reserve, said in early May that it remains on track to lift interest rates in the second half of the year. If so, Norway would be the first major currency to move its rates higher.

And that’s great news for us.

Currencies trade in pairs, as though they’re on a seesaw (one goes up, the other must go down, by definition). And they very often make fundamental moves relative to each other because of something called “the carry trade.”

Simply, if the krone pays a higher interest rate than, say, the dollar, then investors sell the dollar to own the krone. They basically earn free money from the higher interest. And selling the dollar and buying the krone, means a higher krone relative to the dollar.

Right now, Norwegian rates sit at 0%, while U.S. rates are 0.25%. Assuming Norway lifts rates by 0.25%, then it will be on par with the U.S.—and tilting the favor toward the krone is that Norway is a big oil-producing economy at a time when oil prices are rising, plus the country has some of the strongest fiscal fundamentals in the world. Government debt as a percentage of the overall economy doesn’t even reach 31%. The U.S. is approaching an astounding 130%, a crippling level that will weigh heavily on the dollar over the course of this decade.

If the Norges Bank follows through on its vision and pushes Norwegian rates to 0.75% by the end of 2022, our krone position is in great shape to ride higher over the longer term. We definitely should have a pretty good second half of the year as the global currency markets react to Norway’s first rate hike.

Keeping with Norway for a moment, Yara International, another commodity/inflation play tied to industrial and agricultural chemicals, is up around 9% for us so far. More relevant to this update, however, is that Yara paid us our 10 krone per share dividend (about $1.20) in late May. So, if you own Yara and you haven’t looked at your portfolio in a few days, you should see a dividend payment.

Yara also announced in early May that it will buy back up to 5% of its outstanding shares over the next year. That will shrink the share base, which has the effect of spreading the company’s profits over fewer shares. All things equal, that’s a positive for the share price going forward.

As for our positions in the Swiss franc and the MSCI One Belt One Road ETF (our play on emerging markets winning the commodity super-cycle), these remain stable. We’re up about 2% in the franc and 4% in the ETF, which we’ve only owned for a month.

The franc has been slowly strengthening against the dollar, which is precisely as I would expect. The franc isn’t going to sharply lurch higher or lower, except in a global crisis (which would see it spring higher). Instead, it will drift.

The Swiss central bank, however, is struggling a bit with this recently because a strengthening franc makes life more expensive in Switzerland and reduces the country’s economic competitiveness.

So, I would not be surprised if Swiss central bankers start buying up dollars by selling the franc. That would weaken the franc a bit. But it’s a bit like pouring a gallon of water into a swimming pool—it will make a small difference, but not a long-lasting difference. The franc is simply headed higher versus the dollar as the rest of this decade unfolds.

This month saw the launch of the Global Intelligence Crypto Intelligence Library and the addition of seven new positions to our portfolio—my four recommended cryptos, two crypto stock recommendations, and my recommended crypto interest account. (If you haven’t had a chance to peruse the library yet, you can download and read my four reports on bitcoin, Decentralized Finance, crypto gold, and crypto privacy in the Library tab on the members’ area of our website or by clicking here.)

So in keeping with the expansion of our portfolio to the crypto realm, I want to spill a bit of digital ink on our new crypto positions.

You have, no doubt, seen or heard about the craziness in the crypto market of late. And that’s what I really want to address. First and foremost, crypto can—and regularly does—move with whiplash volatility. Which leads to the most important message I can share with you: Invest only what you are comfortable losing.

Frankly, I don’t believe total loss is a real risk. The cryptos we hold are high quality.

Bitcoin has clearly taken shape as a store-of-value. Ethereum is becoming the most important, necessary network for running blockchain services (as I point out in your DeFi report, it’s like owning the tracks on which all the trains run).

Aave is a leader in the DeFi space and will continue to vacuum up assets as DeFi explodes in size. And Band Protocol offers a service—pulling real, physical-world data onto the digital blockchain—that is an absolute necessity for DeFi as it reshapes all of personal finance.

So, truthfully, I’m not worried about the volatility inherent in crypto. But you need to be comfortable with it, too. And if you’re not, that’s OK. Don’t own volatile crypto, if it makes you queasy. Instead, stick to stablecoins (which I also explain in the DeFi report) and collect 8.6% annual interest income with no volatility to cause you sleepless nights.

Personally, I think the gods of crypto smiled on us and sent us a sell-off just so we could buy high-quality crypto projects at fantastically cheap prices. We officially launched a position in bitcoin at less than $40,000 and Ethereum at less than $2,500. Bitcoin will very likely see six figures this year, and seven figures in the next few years. Ethereum will grow 10 times from here, probably more, over the next few years.

As for Aave and Band…both have big upside. We’re into Aave for under $375, and I would not be surprised to see it double fairly quickly (by end of summer) as the crypto market rebounds. Aave was a nearly $650 token before the recent lunacy. It will march right past that level.

Band was recently north of $20 and we got in at a price of just over $8. As such, I expect Band will triple in price in short order as it climbs back into the $20s.

I write this with such confidence because of what I see happening.

First, the blockchain is a game changer—full stop. It is changing the way the world works by making processes and services more efficient and less costly. It’s transformational. We are very—very!—early into that process. Vast wealth will be made as all of this unfolds.

Second, the sell-off was a manipulation. Thing is, we can literally follow the money because the blockchain records everything for everyone to see. And during the sell-off, the biggest sellers were accounts that had held bitcoin for just days to a couple of weeks. That’s odd. Who buys bitcoin to immediately sell it?

Institutions that already own scads of bitcoin but want more. It’s a simple game. Accumulate some bitcoin over a few days or weeks and then suddenly dump all of it in one fell swoop. The selling pressure is greater than the buying pressure, and it feeds on itself, causing the price to collapse amid a bout of retail-investor fear.

And then what do you do? You wade into the bloody mess you created and grab lots of bitcoin on the cheap. Which is exactly what was happening, since institutions were actually buyers during the bloodshed.

The fact is bitcoin is a limited-quantity asset. Glassnode, one of the most-respected crypto research firms, reported earlier this year that only about 4.2 million bitcoin are available for trading. The other 14.5 million that currently exist are locked away in digital wallets (and about 20% of those are considered forever lost because owners forgot passwords or passed away).

That means investors—particularly institutions—are grappling for control of a tiny quantity of bitcoin. Institutions know exactly where bitcoin is headed (seven figures) and they want as much of it as they can grab. And what better way to shake free some bitcoin than by creating an artificial plunge, scaring away the newcomers who have only been buying in the last several months, and snapping up the bitcoin they’re getting rid of?

Sounds conspiratorial, I know. But, like I said, the blockchain is open to all, and the data show that institutions were gobbling up bitcoin in the sell-off. They won’t shake me out of my position, I can promise you. And I hope you use this opportunity to buy bitcoin before its truly epic run begins.

Rich Waryn has over 30 years’ experience in international private equity fund management, real estate investment, and entrepreneurship. He resides in Colorado where he is managing director at a national investment bank and owns a specialized transportation logistics company.

You might imagine that the more money you make as an investor, the more tax you have to fork over to dear old Uncle Sam.

Except, of course, that’s not necessarily true.

Savvy investors take a page out of the playbook of the uber-rich and use a variety of legal strategies to lower or even eliminate the tax on their gains.

And few investment sectors give you more opportunities to grow your wealth without paying capital gains tax than real estate.

I by no means consider myself among the uber-rich, but I certainly know how this world operates. During my career, I have led a variety of investment firms and helped launch billion-dollar infrastructure investment funds.

Today, I am owner and president of a logistics company in Colorado and managing director at ACT Capital Advisors, a national investment bank.

Over the years, I have invested a lot of my personal wealth in real estate.

Through these investments, I learned to use a tax rule available to all real estate investors that can cut your long-term capital gains tax bill to zero.

This strategy has been criticized as a loophole, and aspects of it are currently in the crosshairs of the Biden administration. But as of right now, this rule is still in effect and for my money, it is one of the keys to getting rich through real estate investment in America.

In the right circumstances, it can even allow you to turn the equity you own on an investment property into a monthly income that requires zero management on your part…a dependable income that you could use to fund a new life or retirement overseas.

This strategy is called a 1031 exchange.

If you’ve ever bought an investment property, the term “1031 exchange” might be familiar to you. Of the many tax reduction and elimination strategies in the real estate space, it is among the most effective.

Named for section 1031 of the tax code, this rule allows sellers of U.S. investment properties to defer capital gains tax indefinitely by buying another property or properties of equivalent or higher value.

This rule has been part of the U.S. tax code since the 1920s and originally covered the exchange of all sorts of investment assets, like machinery and livestock. Today, it is exclusively in the realm of real estate investment. Here’s an example of how it works:

Say you bought a house as an investment property some years ago for $400,000. Since then, it has risen in value to $600,000. Your outstanding mortgage is $200,000.

Now, you’ve spotted an opportunity to invest in a new property, costing $800,000, that will generate significantly higher income.

If you were to simply put your current investment property on the market and sell it for cash, you’d face a hefty bill, since you’d owe tax on your gains of $200,000. (For simplicity, I’m excluding depreciation, closing costs, and a host of other factors that in reality would affect the final taxable amount.)

Given that the long-term capital gains tax rate in the U.S. is as high as 20%, depending on your income level, you might owe Uncle Sam as much as $40,000. And that’s before local taxes and surcharges are included.

However, if you use a 1031 exchange to swap your current investment property for the new one you’ve identified, you can defer your capital gains tax bill entirely.

One of the rules of 1031 exchanges is that if you have a mortgage on your original property, you’re basically required to replace the value of this debt…typically with a new mortgage or personal savings.

So, you could take the $400,000 profit ($600,000 minus the mortgage) from the sale of your first property, get a new $400,000 mortgage and buy the second property…and owe little or no capital gains tax.

To qualify for this kind of exchange, the properties must be considered “like-kind” by the IRS. However, this term is not as restrictive as it sounds. In reality, the application of this rule is quite liberal, and the investment properties can differ in grade or quality.

You could, for instance, swap a piece of vacant land for an apartment, a business premises for a condo, or a farm for a house. You cannot, however, conduct a 1031 exchange with a new investment property located outside the U.S.

The 1031 exchange rule can also be used for consolidation or diversification, meaning you could swap one property for several, say one home for a number of condos, or vice versa. And you can do this as many times as you like.

When you ultimately cash out, you will of course have to pay long-term capital gains tax.

So, if over the course of your real estate investment career, you managed to turn an initial $200,000 investment into $2 million worth of property by using 1031 exchanges, you would owe long-term capital gains tax on $1.8 million if you cashed out.

However, many real estate investors choose to pass on their investment properties in their wills, since current tax law allows your heirs to receive the property on a “stepped up basis.”

This means that the tax basis is automatically stepped up to current market value, so in the case of our example, $2 million. Your heirs could then sell the property and pay little, if any, tax. So, in essence, you may never have to pay long-term capital gains tax on real estate.

That is not to say, however, that 1031 exchanges are easy or simple to enact. The rules are complex, so you’ll need a tax professional to help you navigate them.

The biggest issue you’ll likely face is finding a property within the allotted time frame.

You have up to 45 days after you sell your investment property to identify the property or properties you want to use for the exchange. You then have 180 days to close the sale on the new building. (These times run concurrently.)

While you seek to complete the new sale, the funds from the original sale are held by a 1031 exchange intermediary. These are specialized individuals or companies that focus exclusively on ensuring that all the 1031 requirements are met. Intermediary fees are usually pretty reasonable (under $1,000).

If, for whatever reason, you fail to complete the sale in time, the 1031 process is canceled. The intermediary will send you the proceeds held in their account and you will owe capital gains taxes.

For this reason, one of the key stumbling blocks for many sellers is actually finding a property of equal or greater value that meets their needs, while also meeting the requirements of a 1031 exchange.

For example, I recently sold an office building for $1.7 million that I had bought for around $1 million a few years ago.

Having lost some tenants over the past year, I was concerned about the long-term impact of COVID on the commercial office market. Prior to COVID, I was able to replace these tenants with ease. With the pandemic, I did not receive a single rental offer.

Granted, things are now beginning to return to “normal,” but even so, it appears that many companies, mine included, are deciding that it is easier, and more cost effective, to simply allow their employees to continue working from home.

I received an attractive offer from a company that wanted to convert my office space into a senior daycare facility. So, I decided to sell.

I was able to lower the amount applicable for capital gains by factoring in commissions and other accrued expenses. However, I am still facing taxes on gains of around $500,000.

In order to qualify for a 100% tax deferral under a 1031 exchange, I would need to buy a property valued at $1.5 million. The issue is that I still had about $700,000 in mortgage debt on the building.

That means that I would need to find another building or buildings valued at $1.5 million or higher and take on another mortgage of at least $700,000, or pay the difference in cash. And all this needs to happen within the relatively tight time frames provided for by the law.

After surveying the market, I quickly realized that there were no attractive options in my area that met the requirements I was looking for.

That’s when I decided to have a look at another option available under the 1031 exchange rule—something called Delaware Statutory Trusts (DSTs).

DSTs are legal structures that meet the requirements for the federal 1031 tax statutes. Basically, instead of buying a particular property, a seller can invest in a qualified property fund.

These funds are typically run by a management company that invests in multiple properties, thus spreading risk while providing potentially attractive returns. Often, DSTs have specific themes such as hospitality, commercial offices, or industrial or medical facilities.

Investors can review fund prospectuses as they would review the prospectus for a mutual fund. The difference is that these funds are not typically listed on exchanges; they’re more akin to private equity investments.

DSTs will provide details of the types of real estate they invest in as well as the amount available to invest, minimum investment size, projected annual income returns and total returns, and very importantly, leverage levels…meaning the level of debt.

That last point was key for me (as it is for most real estate investors, who often have some level of debt associated with their properties). It basically means that I can put all of the cash proceeds from the sale of my building into a DST with the right leverage level and not have to worry about taking out any more loans. The loans are already baked into the fund structure!

As with most things in life, there is a flip side to DSTs. Often, the groups that buy real estate and then convert to a DST will mark up the value of the properties by 10% to 20%. In addition, they will also charge management fees and take a share of the profits.

As a former private equity fund manager, I understand this concept well. The fund managers are creating value and should be appropriately compensated. The big question is, what is “appropriate?”

Traditionally, private equity firms have worked on a 2/20 structure, meaning they take an annual fee totaling 2% of assets under management, plus 20% of the profits after exits are completed and after the investors get 100% of their money back. So, DST fees should be in this range.

The other important point about using a DST is that you typically need to be considered an “accredited investor” to qualify. These funds are private offerings and fall under specific SEC guidelines. To be considered an accredited investor you would need to meet one or more of the following criteria:

Still, if you have the ability to move your equity from an investment property into a DST, they can be an excellent way to generate passive income. This makes them very interesting propositions for those approaching retirement.

With DSTs, the managers collect rents, deduct operating expenses, and then pass on the net income, less a reserve, to investors…generally on a monthly or quarterly basis.

This feature can be especially attractive for those who want a stable income to help fund a new life or retirement overseas.

It is important to note, however, that the monthly cash flow is considered to be ordinary income and is taxable in the year that it is received.

Another important point is that the funds eventually sell their properties and distribute capital gains. This means that in five or 10 years (or whatever the life of the fund is expected to be), there will likely be another capital gains event and the need to do another 1031 exchange.

Alternatively, you can just decide to pay the capital gains tax at that time.

That’s actually a calculation I am making right now. At 20%, the long-term capital gains rate is probably as low as it will be for a long time.

Under the Biden administration’s proposed budget, released at the end of May, the top rate of capital gains tax would jump from 20% to 39.6%.

When you include the 3.8% Medicare surtax on high-earners in effect since the enactment of the Affordable Care Act, this would push the top rate of long-term capital gains to 43.4%, making it higher than the top rate on salaried income.

The administration has similarly proposed eliminating 1031 exchanges on transactions with profits exceeding $500,000.

Also in the suggested budget are plans to amend the step-up-in-basis rule—the regulation I mentioned above that allows heirs to inherit investments without having to pay long-term capital gains tax.

Under the proposals, this rule would be eliminated, with an exemption of $1 million per individual plus $250,000 for a primary home. (For married couples, the total exemption would be up to $2.5 million.)

All of these tax policy changes would have to be approved by Congress, so they are by no means certain to come into effect. However, some tax increases appear likely.

So, for high-income earners who’ve been considering cashing out on an investment property, this could be an opportune moment to act.

However, property investment is not only the realm of the very wealthy.

Demand for second homes spiked by 100% between October 2019 and October 2020, according to a study by real estate brokerage firm Redfin. With mortgage and interest rates at or near historic lows, a lot of people decided that property was a sound investment asset.

Plus, 1031 exchanges are commonly used by smaller investors. A 2020 survey from the National Association of Realtors revealed that about 12% of real estate sales between 2016 and 2019 were part of a 1031 exchange, and of these 1031 exchanges, 84% were by smaller investors.

So, if you’re among those who jumped into real estate investment in recent years, or even if you’ve ever considered dipping your toes into this sphere, know that you have ways to alter and upgrade your portfolio…without getting hit with a big tax bill.

In a previous issue of the Global Intelligence Letter, I mentioned that when I’ve got a little downtime, I like to scroll through websites that show listings of turnkey businesses overseas.

In my global travels, I’ve encountered numerous expats running successful businesses…the kind of ventures you fantasize about owning. I once met a 50-year-old Brit in a tropical bar along the Mekong River in Phnom Penh, Cambodia, and it turned out he owned the place.

Then there was the photographer from the Northeast who started her own art nonprofit in Uruguay. And the guy from the Midwest who opened a barbecue and wine restaurant in northern Argentina. There are others…

So, I know from interviewing people I’ve come across that an engaging, fulfilling business overseas can be more than a daydream; it can be your reality.

Now, as the world prepares to reopen, I thought it might be fun to share some of the interesting listings I’ve recently happened upon. Of course, I haven’t vetted these; they’re not recommendations. Just a bit of escapism and a window into the myriad possibilities.

With tourism businesses struggling for obvious reasons over the past year or so, you can find countless hotels and bed-and-breakfasts for sale online.

Most look like a grind rather than the kind of relaxing business you’d dream of owning, but I did stumble across this offering in Olhao, a municipality in Portugal’s gorgeous, sun-kissed Algarve region.

Located in the countryside, the B&B has six guest suites and a separate house for the owners. It also has a pool, and is within a short drive of town and the beach. The price: €795,000 ($970,000) and for that, you get everything, including furnishings and the website.

If you prefer something a little less sedate, how about a horse tours business in Costa Rica?

Located near Jaco Beach in Puntarenas, the company on offer is situated on 35 acres of pasture land and more than 40 acres of jungle trails. It has been in operation for a good length of time, 14 years, and is mentioned in the country’s Lonely Planet guide.

The business comes with 11 horses as well as a bodega, ranch, and several vehicles. And the price is a very affordable $185,000. Check out the listing here.

On the opposite end of the affordability spectrum, how about owning a sprawling farm and vineyard in Italy?

For a cool $3 million, this place would have to be pretty special…and to be fair, it looks quite spectacular. Set in the hills of Siena, the property spans 25 hectares, two of which are dedicated to olive groves with about 600 plants. The vineyards, meanwhile, cover around 1.7 acres and currently produce upwards of 5,000 bottles of wine a year.

The main building is a 17th-century farmhouse with traditional Tuscan features like terracotta floors and is divided into four apartments, with independent kitchens. There are also two other apartments in an adjacent building as well as a garden with a swimming pool…meaning the property could work as a tourism business.

■Earlier this month, I instantly turned $250 into tens of thousands of dollars. Here’s how…

A while back, I joined a cryptocurrency site called CoinList. It hosts initial coin offerings for new cryptos, something similar to initial public offerings in the world of stocks.

As a member on the site, I can enter a lottery to buy newly listed cryptocurrencies. And let me tell you, these things can truly skyrocket…jumping in value by huge multiples as soon as they list.

For this reason, the lotteries are extremely competitive. I’ve actually yet to gain access to one. I was, however, offered an after-listing opportunity to buy a new crypto token called Clover Finance at the initial offering price.

So, I spent $250 buying 1,250 coins at $0.20 apiece. But when I bought them at this price, they were already trading in the crypto market at about $17, so I instantly turned my $250 into about $21,000. As part of the deal, I’m required to hold the tokens for six months. So, who knows? Maybe they drop to zero and I lose my $250. (Amid the recent market lunacy, Clover slipped a bit so that my stake is now worth between $15,000 and $16,000.)

But I did my homework and I believe Clover has a solid project in the crypto space.

Now, before you rush off in a fit of excitement and join CoinList, I have some unfortunate news. The ICO listings on the site are not currently open to Americans. I was only able to gain access because I’m a resident of the Czech Republic, with proof of that.

So, if you have residency or citizenship outside the U.S., I’d certainly encourage you to sign up. But if you’re in the States, you’re locked out for now.

That’s the really unfortunate thing about the cryptocurrency space. Americans are prevented from accessing so many opportunities because of the U.S. government’s strict financial reporting requirements. It’s the same with regular banks and brokerages around the world. Many will simply not accept Americans as clients for this reason.

I’ll be keeping a close eye on the situation with CoinList and let you know if this rule changes.

In the meantime, I’d still advise that you take a look at the platform. The site is not available in Alaska, Hawaii, Minnesota, Nevada, or New York, but you can trade crypto on it in the other 45 states.

And when I checked just recently, it was offering 17.9% interest for staking the TerraUSD (UST) stablecoin. (Staking means locking away your crypto for a set amount of time, like putting your dollars in a certificate of deposit. See your DeFi report for a full explanation of stablecoins.)

TerraUSD, by the way, has a market capitalization of $2 billion, so it’s not some brand-new, here today, gone tomorrow crypto. This just illuminates the scope of opportunities in the cryptoconomy and I’ll be bringing you more on all of this in upcoming issues.

■PayPal just announced a major change to its crypto policy.

Since 2020, PayPal has allowed users to purchase major cryptos like bitcoin through its platform. However, I advise against using PayPal to buy your crypto for a few reasons.

First, the selection of coins is extremely limited; PayPal offers only four cryptos at present. An even bigger concern—and one I outline in my bitcoin report—is that you can’t withdraw your cryptos…which in turn means you can’t deposit them with a company like BlockFi that pays interest on major tokens like bitcoin and Ethereum.

Now, however, PayPal is changing its position on withdrawals.

The global payments giant recently said that it plans to let users withdraw cryptocurrency to third-party wallets. There’s no announcement yet on when this will happen. And even when it does, PayPal would have to make a lot of other improvements to catch up with my preferred exchanges, Binance.US and Coinbase, including dramatically expanding its crypto offerings.

Still, the fact that a major service like PayPal is going to allow withdrawals means it recognizes the potential of DeFi and crypto interest accounts. In fact, I wouldn’t be surprised if PayPal’s real goal is not allowing withdrawals, but enabling deposits…so it can build its own DeFi business.

■The dollar collapse is gathering pace…

In the March issue, I warned about the forthcoming fall in the value of our dollars and the impact this would have on our purchasing power since we import so many goods from overseas.

Well, as anticipated, the dollar has been sliding lower. Near the end of May, the Dollar Index, which measures the greenback against a basket of world currencies, hit a six-year low.

Alas, this is not a trend we can expect to turn around anytime soon.

As I mentioned in March, I anticipate the Dollar Index will continue falling until late in this decade, and drop almost 50% from its current level. Of course, there’s nothing you or I can do to prevent this, but we can take steps to protect our purchasing power by moving some of our wealth into assets that rise as the dollar declines.

The recommendations in the March edition and this issue, in particular, will help in this regard.

■You could win up to $1.5 million for getting your vaccine shot if you live in one of these states.

To encourage COVID vaccine uptake, a host of U.S. states are running prize drawings for recipients.

Among those with the biggest prize pools, Maryland is holding a drawing each day from May 25 to July 3 in which one person will receive $40,000. Then, on July 4, a final drawing for a $400,000 prize will take place. And all residents who have gotten one dose are automatically entered.

On the West Coast, Oregon is staging a $1 million cash prize drawing on June 28 for residents who’ve received at least one dose by the previous day, while California plans to give away $1.5 million prizes to 10 residents on June 15. Anyone over 12 who has not yet been vaccinated or has only had one dose can apply to the California lottery.

Meanwhile, Ohio and Colorado are both holding five drawings for $1 million prizes.

■Do not buy a used car this year (or even next year) if you can avoid it.

Last month, the average cost of a used car in the U.S. topped $25,000 for the first time in history, according to research firm J.D. Power, with car prices jumping 10% in April alone.

I’ve been harping on about an impending inflation crisis for months. Besides the dollar slide, it’s the other major economic cloud looming overhead. That means the prices of most goods will continue to rise. But that’s not necessarily true with cars…

The price surge in used cars is primarily related to a global computer chip shortage. This in turn is a result of the pandemic, a fire at a major Japanese plant, and the severe winter storms in Texas, which shuttered several chip factories in Austin. Cars today are filled with computer components, meaning car-makers can’t make new vehicles without processors, and this is pushing the prices of used cars higher.

The chip shortage is going to continue for some time, but it also won’t last forever. So if you can put off buying a new or used car until next year, or even the year after, you’ll likely get a much better deal.

■Here’s a controversial way to save big money on flights.

Another area where you’re likely to see elevated prices in the coming months is flights, as travel patterns begin to return to their pre-pandemic norm. However, there may still be a way to find some bargains…if you use a controversial practice called skiplagging.

Skiplagging is the process of buying a multi-flight ticket that transits through the destination you actually want to visit. Then instead of getting the next flight, you simply get off at the connection point, rather than continuing on. Because of the curious ways the modern aviation industry operates, this can actually cost you less than simply booking a direct ticket to your destination.

The practice is not new. Nor is it illegal. But airlines hate it and it is against the terms and conditions of their loyalty programs. So, it’s best not to do this regularly, or use this on any airline with whom you have air miles or other bonuses. Moreover, when you skiplag, you can’t check any bags.

However, if you can’t find a regular flight at a reasonable rate, it’s worth checking what a skiplagged flight would cost you, because the bargains can be truly astonishing. You can search for flights of this kind at Skiplagged.com.

■Help fight cancer and coronavirus while you sleep.

One of the biggest barriers to experimental medical research is computing processing power. Not every scientist has access to a supercomputer, and analyzing large, complex data sets on standard commercial computers can take years. That’s where you and I come in…or rather our smartphones do.

DreamLab is a specialist app that uses the processing power of smartphones to help analyze complex data while their owners sleep. Developed by the foundation of international telecoms giant Vodafone, it uses a network of smartphones to power a virtual supercomputer that can process billions of calculations.

The app was originally used to aid cancer research. But following the COVID outbreak, a new Corona-AI project launched on DreamLab. Under this program, which is organized in partnership with Imperial College London, the app is now also being used to find anti-viral treatments for COVID. So basically, this is an easy way to help tackle two of the most serious medical problems on Earth, without lifting a finger. All you have to do is install the app and charge your phone while you sleep.

DreamLab never accesses personal data of any kind. To date, it has been downloaded more than 1 million times and currently uses the processing power of about 250,000 smartphones. You can join the fold by downloading the app for your Android or Apple device.

Thanks for reading and here’s to living richer.

Jeff D. Opdyke, Editor

Global Intelligence Letter

© Copyright 2021 by International Living Publishing Ltd. All Rights Reserved. Reproduction, copying, or redistribution (electronic or otherwise, including online) is strictly prohibited without the express written permission of International Living, Woodlock House, Carrick Road, Portlaw, Co. Waterford, Ireland. Global Intelligence Letter is published monthly. Copies of this e-newsletter are furnished directly by subscription only. Annual subscription is $149. To place an order or make an inquiry, visit www.internationalliving.com/about-il/customer-service. Global Intelligence Letter presents information and research believed to be reliable, but its accuracy cannot be guaranteed. There may be dangers associated with international travel and investment, and readers should investigate any opportunity fully before committing to it. Nothing in this e-newsletter should be considered personalized advice, and no communication by our employees to you should be deemed as personalized financial or investment advice, or personalized advice of any kind. We expressly forbid our writers from having a financial interest in any security they personally recommend to readers. All of our employees and agents must wait 24 hours after online publication prior to following an initial recommendation. Any investments recommended in this letter should be made only after consulting with your investment adviser and only after reviewing the prospectus or financial statements of the company.