Dear Global Intelligence Letter Subscriber,

It looks like any typical community in America…

Rows of nice, neat houses set on small parcels of land, each with a lush green lawn.

The supermarket is over on First Street. Opens at 9, closes at 7 most nights. Nearby is the fire station, a hotel, and a gym.

A few minutes away is a small country club with an 18-hole golf course and a restaurant that rates #1 in the region. The elementary school is named for a local man who claimed he was descended from a king… and who was ultimately executed for treason.

Aside from that treason stuff, it feels just like small-town America.

Only this community isn't in the States.

It's high in the desert mountains of Peru.

The town, called Villa Cuajone, is in the far south of the country, where the Andes enter Peru after leaving neighboring Chile. It's a tiny little place. Population: Less than 400.

It's what Americans would've once called a "company town"—those communities that sprang up around new factories in the 1940s and '50s, often funded by the company so workers and their families had a place to live close by.

The only reason this little oasis of green lawns exists is because of a company that arrived in the area decades ago to exploit the vast riches of the Andes… an embarrassing wealth of copper.

So much of the metal hides in the local Andes ore that Peru ranks #2 in global copper mining… providing fully 10% of the world's production capacity.

The country is also #2 in terms of copper reserves, trailing only Chile, according to the U.S. Geological Survey. All told, the Peruvian Andes are thought to contain more than 81 million metric tons of copper, 9% of the world's known reserves.

As you've likely surmised, that metal—copper—is the focus of this month's issue of Global Intelligence.

Copper is a key input in green energy technologies. With every major economy rapidly racing toward green tech, the world will require more copper over the next decade or so than all the copper that was consumed over the last 120 years.

That speaks to a reality I've been writing in Global Intelligence and my daily Field Notes columns… that the green energy embrace is happening far too quickly to be practical. So quickly, in fact, that it's likely to cause a global energy crisis.

But it's happening nevertheless. Too much political, social, and financial capital has been expended to change course now, despite the crisis to come.

Governments all over the world—led by the U.S., European Union, and even China—are spending trillions upon trillions of dollars to usher in a zero-emissions future.

This future will be defined by electric cars… solar and wind farms… new nuclear plants… electric airplanes… and a wide range of technologies to generate power from algae, tides, and other sources that don't originate with dead dinosaurs.

It's a multi-decade process. After all, it takes years to build new power plants. Similarly, the global auto fleet cannot be switched to electric and hybrid vehicles overnight.

Across the coming decades, a variety of companies and industries will reap vast riches from this green transition.

But perhaps no industry is sitting prettier than the dirty ol' business of copper mining.

Copper is the single-most efficient metal for electrical conduction. As such, it's an essential component in pretty much everything that electrifies our world.

As we progress full speed toward greening the global economy, copper has a decades-long tailwind fueling its price.

So, with this month's issue, we're going to benefit from that trend by looking to the company that founded Villa Cuajone… a copper-mining giant whose stock could double in price as the green revolution gathers steam.

Villa Cuajone in southern Peru. © Gonzalo Alfaro Puma

Working-Class Gold

Global governments today seem trapped in a hedonistic pursuit of unrealistic green energy mandates.

One example of what I mean: The Biden administration has announced a plan to have the American government running on 100% carbon-pollution-free electricity by 2030. That means more than 300,000 federal buildings must be connected to power plants that produce no emissions in the generation of electricity.

It's a noble goal to be sure, but the lunacy of the timescale is right there in the numbers…

Those 300,000 buildings are spread all over the country, which means they are connected in some way to many of the nation's 11,925 power plants that produce at least 1 megawatt of electricity.

In effect, then, the plan would require the rapid construction of new clean energy plants, and it would mean that thousands upon thousands of existing plants must switch to some form of zero-emissions fuel. Even if that's just half of those 11,925 power plants (and it's likely more), it means plants must be converted to clean energy at a rate of more than two per day… every day… for the next seven years.

That's patently unachievable. But it's not going to stop government and industry from at least trying.

They will undoubtedly manage to convert some of the plants. And in that transition, a lot of wealth awaits those who own copper mines.

See, while numerous metals can serve as electrical conductors such as silver, gold, and aluminum, copper has them all beat.

Pure silver is the best conductor, but it tarnishes… as anyone with a set of grandma's hand-me-down silverware knows. That tarnish impedes conductivity over time. Plus, at more than $20 per ounce, silver is darn expensive for basic wiring needs.

Gold is far less resistant to tarnishing, and it remains conductive for a longer period of time. But if silver is a pricey metal for wiring, then electrifying a house with gold at nearly $1,900 per ounce would cost a king's ransom. A typical house consumes 439 pounds of copper for wiring. Replace that with gold and the wiring alone costs more than $13.3 million.

Aluminum was a popular wiring metal back in the '60s and '70s. It's incredibly cheap and malleable. But it has the nasty habit of expanding and contracting, and it can deteriorate over time, becoming a fire hazard.

The rest of the metals—zinc, brass, bronze, lead, iron, etc.—are increasingly less conductive and less easy to install.

That leaves copper.

It's cheap—about $1,700 today for that 439 pounds needed to wire a typical home.

It's highly conductive, second only to silver in efficiency.

It's highly ductile, meaning wiring can easily be bent into whatever shape is necessary.

And it's resistant to heat so the wires aren't a fire hazard.

As such, copper is one of the basic building blocks of an industrial society. I like to think of it as working-class gold.

The metal these days goes into everything from tubing for water pipes and refrigeration lines, to electrical wiring, smartphones, TVs, industrial machinery, airplane hydraulics and navigation, and even medical products. (Environmental Protection Agency research indicates that copper surfaces can kill 99.9% of bacteria within two hours.)

All of those use-cases expand as global GDP grows. So, anyone who believes the world economy is going to grow larger over time is reflexively bullish on copper.

Moreover, as the fight to eradicate fossil fuels accelerates, copper usage will ramp up at an almost exponential pace.

The current replacements for fossil fuel-powered cars and power plants are well-known to us: wind and solar, nuclear energy, and hybrid and full-electric vehicles.

Others will come in time, including tidal power and hydrogen-fueled cars, trucks, and planes.

All of those technologies—those readily available today and those coming-to-a-future near you—demand massive quantities of copper.

The irony in all of this is that copper mining, like all mining, is a damn dirty business. This points to the dark underbelly of the environmental movement's lust for green energy.

Study after study has shown that copper mines have severe impacts on drinking water aquifers, farmland, animal habitats, and public health. But many in the environmental crowd would be happier if we simply ignore that inconvenient reality.

And so, the pathway to the green future lies through an explosive growth in copper mining.

The Linchpin of the Green Transition

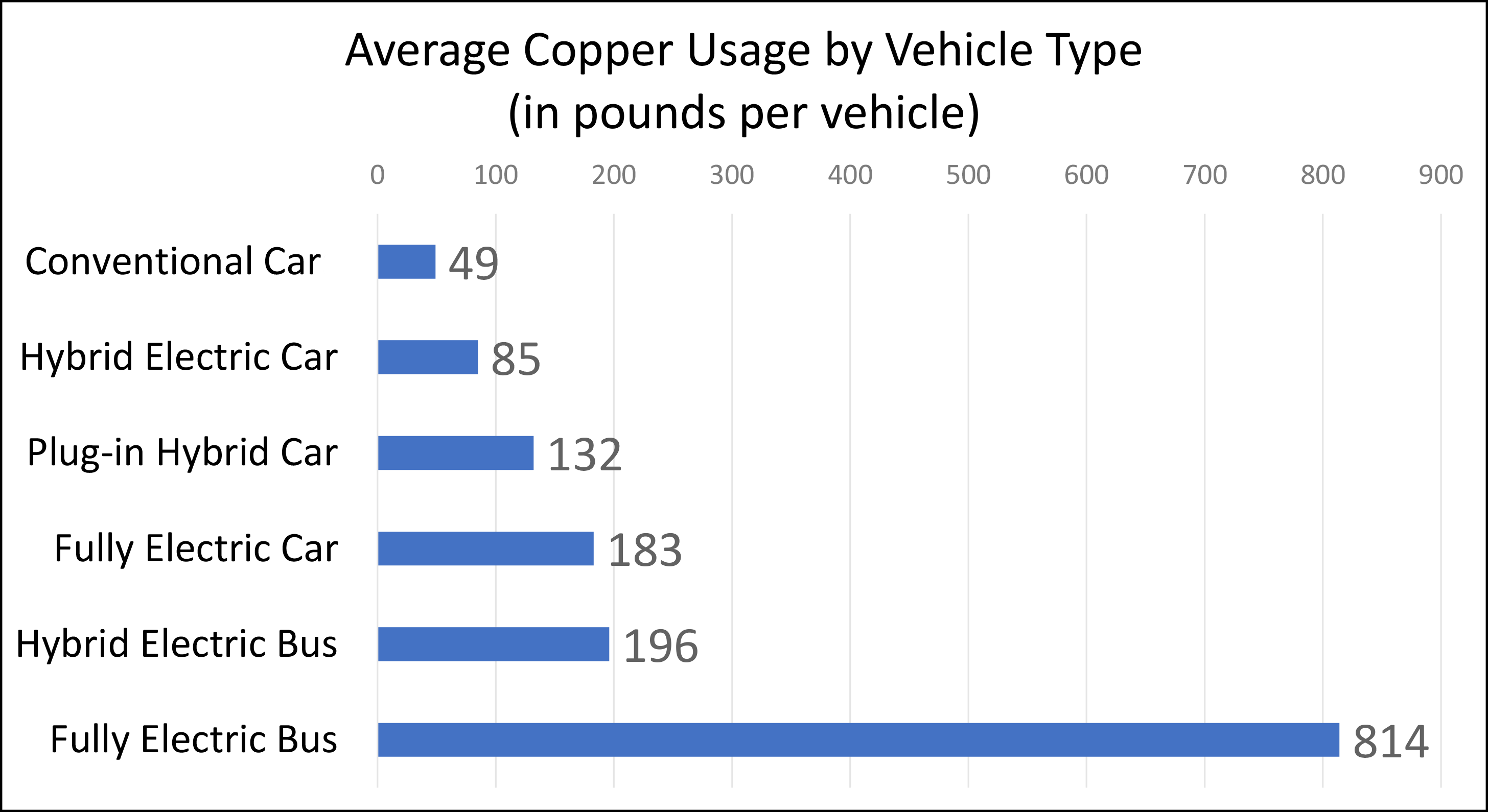

Hybrid and fully electric vehicles provide the perfect example of how copper demand will soar as the green energy transition gathers pace.

The chart below shows how much copper is used to manufacture these vehicles in comparison to traditional, fossil fuel-powered options. These data points on copper consumption come from the Copper Development Association, the engineering and information services arm of the copper industry:

Copper demand from the electric-vehicle market alone is projected to hit 3.7 billion pounds by 2027—up from roughly 500 million pounds today. That's a more than 7x increase in just four short years from now.

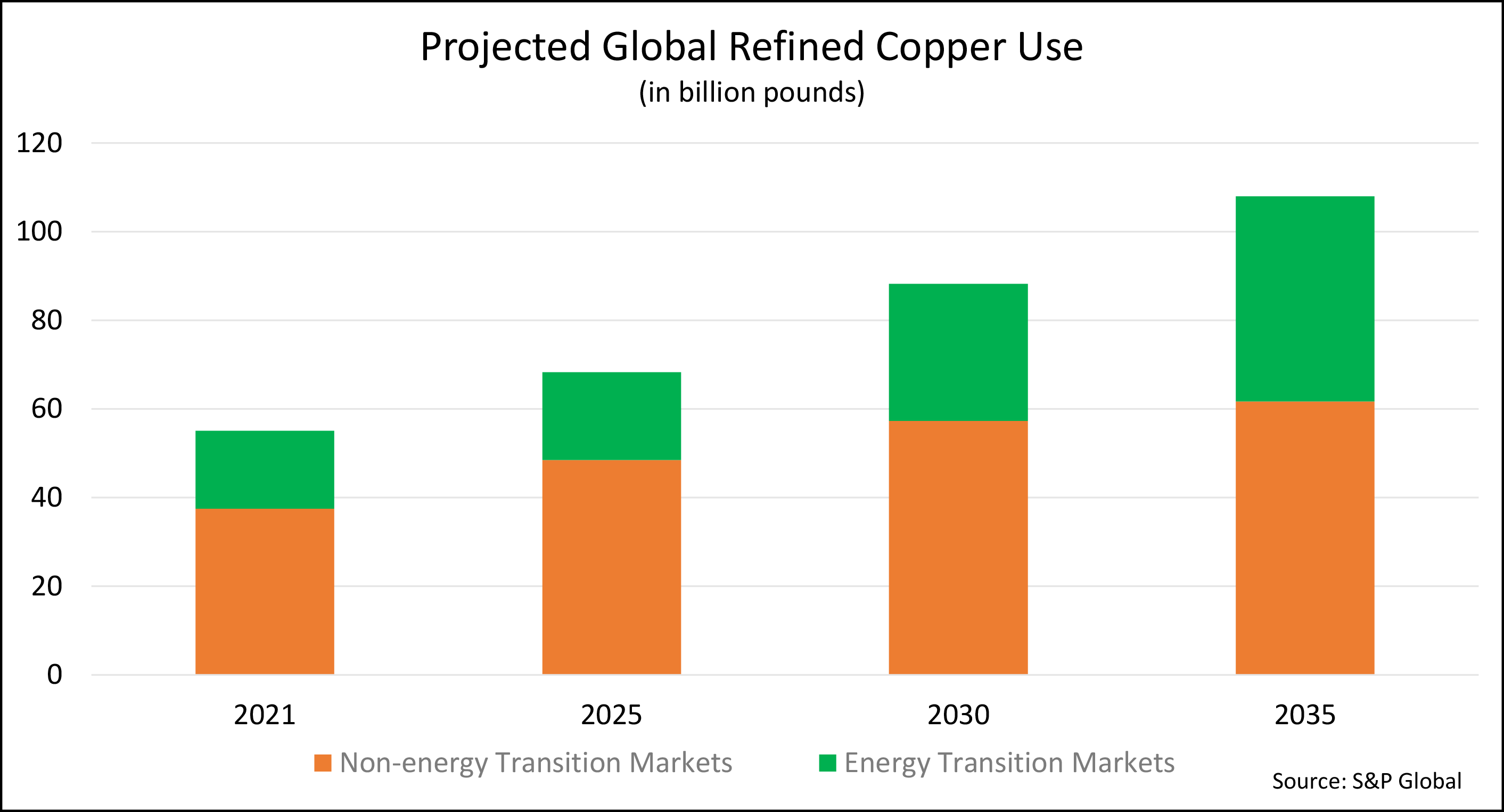

In total, the world consumed an estimated 51.8 billion pounds of copper last year.

Rewiring the world's electricity demands is projected to consume nearly 80 billion pounds of copper by 2030—1.5x the world's total annual usage today for everything that copper goes into.

I won't drown you in a sea of numbers with all the other industries. I will just tell you that S&P Global, the company behind the S&P 500 and a well-respected provider of financial information, projects that by 2035, global copper demand will more than double from today's levels to around 108 billion pounds per year as the world pursues green energy in all its various forms.

Daniel Yergin, a vice chairman at S&P and one of the world's foremost experts on energy markets, says that the green energy transition "is going to be dependent much more on copper than our current energy system."

Yergin also noted that the projected annual demand of 108 billion pounds means that, cumulatively, the world will consume more copper out to 2035 "than all the copper consumed in the world between 1900 and 2021."

Indeed, in a report late last year, Wood Mackenzie, one of the world's most respected energy research and consultancy firms, noted that green energy puts such a demand on copper that "the investment required" for new production "needs urgent attention."

"To successfully meet zero-carbon targets, the mining industry needs to deliver new projects at a frequency and consistent level of financing never previously accomplished," according to Nick Pickens, research director of copper markets at Wood Mackenzie.

Therein lies the problem… and our opportunity.

At this point, it's unclear if it's even possible to mine 108 billion pounds of copper per year.

The world's current mines, along with recycling efforts, generate about 61.7 billion pounds of the metal annually. Looking out over the remainder of the decade, S&P and other copper-analytics firms expect we are quickly approaching an inflection point that sees annual copper supply fall short of expanding demand.

Actually, those observers say supply could fall "far short" of demand.

Current trends "could lead to a historic copper deficit," S&P concluded, adding that as demand for green energy continues to expand, the mining industry will be "really put to the test" to supply the necessary quantity of copper.

S&P stressed that this "historic copper deficit" is likely whether we actually hit global green transition targets… or fall short of them and continue as we're operating today.

The challenge with increasing supply is that opening a new copper mine, or even expanding an existing one, requires that companies overcome obstacles ranging from environmental regulations, to infrastructure and labor costs, to the lawsuits that are inevitable from nearby communities or even the green energy crowd (whose demand for clean energy is what's fueling demand for more and more copper).

So, here in the midst of a commodity super-cycle, in which commodity prices are in a long-term uptrend, copper is locked into its own mini super-cycle that will see copper miners profit from higher and higher metal prices… or they'll profit from higher and higher quantities of copper sold.

But there's more to this story than just the ever-expanding green energy market. And it's more timely…

China's Insatiable Hunger for Copper

Since the emergence of the COVID pandemic, China has closed its economy, then reopened it, then closed it again, only to reopen bits and pieces of it, only to then close it.

It's been chaotic. And that's been a big problem for the copper market.

China is the world's largest consumer of copper… because it's both a massive, growing economy and the world's factory floor. The country is not only the #3 producer of copper, it's the leading importer as well.

So, as China's economy has lurched and slipped over the last two years, copper prices have largely followed suit—up, down, up, down.

We're now in an up moment, with copper back near $4 per pound from recent lows last summer below $3.25. The reason: Back in January, China lifted the shutdowns and reopened its entire economy.

In response, Dutch banking giant ING—well-known for its commodity research—wrote to clients that "China's COVID policy change should prove supportive for copper demand in the medium and long term."

Moreover, the bank noted, "We expect prices to continue to recover from the second quarter onwards on the back of improving reopening sentiment and tight inventories."

By "tight inventories," ING is pointing to the fact that global copper stockpiles held by commodities exchanges remain shockingly low.

Copper stockpiles at the London Metals Exchange—the world's leading venue for trading metals—recently totaled just two days' worth of average global use.

Inventories on the Shanghai Futures Exchange and Chicago Mercantile Exchange, the other two big metals exchanges, are also extremely low. Combined, they had just two to three days of average daily use.

That indicates a big price spike is likely… particularly given that China's economy still hasn't fully normalized since reopening from the COVID lockdowns.

Economies, like aircraft carriers, don't turn on a dime.

Assuming the Chinese government doesn't impose new shutdowns, China's economy will spend the rest of 2023 and into 2024 ramping back up to normal.

That will mean significantly rising demand for copper.

If stockpiles dwindle much more, then there would be no "few days of consumption" buffer… and prices would spike.

The Global Infrastructure Boom

Beyond China's reopening, there's another big price pressure on copper: global infrastructure spending.

Western countries in particular are spending massive sums of money to upgrade their infrastructure since much of it is past its original lifespan and increasingly decrepit. Just look at the spate of high-profile train derailments and bridge collapses in recent years.

Every four years, the American Society of Civil Engineers grades America's infrastructure—bridges, rail, water mains, airports, etc. Overall, the grade in 2021 was a very subpar C-.

To address this, President Biden signed a bipartisan bill committing $1.2 trillion to upgrade America's infrastructure. That money is already flowing through the engineering economy.

Over in Europe, meanwhile, the European Union has signed off on the largest infrastructure plan in its history: NextGeneration EU, which aims to rebuild European infrastructure by spending €1.8 trillion (almost $2 trillion) across the 2021-2027 period.

Back in China, the government is looking to spend $2.3 trillion this year alone on infrastructure.

So, the world's three largest economies combined are planning to invest roughly $5.5 trillion on infrastructure in the coming years.

That's a lot of spending.

Which enhances our opportunity in copper since the red metal goes into telecom, electricity, water, rail, and so many other infrastructure applications.

Wrap all these pieces together and it's clear why we want exposure to copper in our portfolio.

Thus, we return to Villa Cuajone and the mountains of Peru…

The World's Most Efficient Copper Miner

Villa Cuajone took root just 10 mountainous, winding miles from the Cuajone Mine, one of the jewels in the crown of Southern Copper Co .

Southern Copper's Cuajone Mine in Peru.

The company built the town decades ago as a place for managers and directors who run the mine to live with their families. Southern Copper wanted the town to resemble a misplaced piece of America: family homes with front and back yards, porches and driveways, all aligned on leafy streets. Aside from the local language and austere geography, Villa Cuajone could easily pass for Anytown, USA.

Southern Copper itself began back in the 1950s as an upstart U.S. miner that signed an agreement with the Peruvian government to develop the Toquepala mine. That site lies just 30 miles as the crow flies from Villa Cuajone, but three hours by car through the Andean terrain.

Toquepala is still an active mine today, producing between 300 million and 500 million pounds of copper per year, the second-most important mine in Southern Copper's portfolio of eight currently producing copper mines in either Peru or Mexico. Cuajone Mine, meanwhile, is Southern Copper's #2 project in Peru, delivering between 300 million and 400 million pounds of copper annually over the past decade.

The company's top-producing mine is the Buenavista mine in Mexico, which yields roughly 750 million pounds of copper per year. That helps explain why Southern Copper today is a New York Stock Exchange-listed company that's predominantly owned by a larger conglomerate, Mexico City-based Grupo Mexico.

Since the 1950s, Southern Copper has grown into one of the world's premier copper miners.

It's ranked #1 in the world for copper reserves. It's also the world's #5 producer, #7 in refinery capacity, and #10 in copper smelting.

Southern Copper averages a 50-year lifespan for its mines, the longest in the industry, and has one of the strongest pipelines of new copper projects in various stages of development.

And perhaps most importantly, Southern Copper has the lowest "cash costs per pound of copper produced" of any major player in the industry. These are the costs necessary to mine and produce copper.

For Southern Copper, that cost was $0.78 per pound in 2022, when copper was selling on average for $4 per pound. The industry average is north of $2 per pound.

After corporate costs and taxes and such, that low cost structure manifested as net profit margins in the 29% range for 2022, a fat number for such an old-economy business.

As copper prices rise, those margins grow ever fatter.

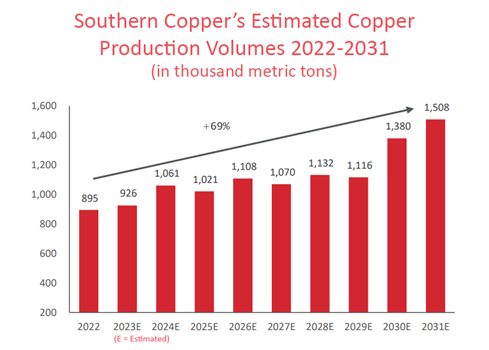

Last year's margins resulted from Southern Copper mining 1.97 billion pounds of copper in Peru and Mexico. This year, company management expects that figure will jump to nearly 2.05 billion pounds.

And based on developments already in the pipeline, Southern Copper expects to be producing more than 2.42 billion pounds, or 1.1 million metric tons, by 2026.

All of that information makes the thesis here really simple…

If you see China reopening its economy… and if you see that the green energy revolution demands vast quantities of copper well beyond what the world now consumes… and if you accept that major economies are spending trillions upon trillions of dollars upgrading and replacing ancient infrastructure… then you are bullish on copper long term.

And if you're bullish on copper, you want to own Southern Copper, little known among most investors, because it's one of the biggest and most cost-efficient players in the industry.

Moreover, Southern Copper is more tightly tied to its namesake metal than any of the other large copper producers.

Other big players in the copper sector (Rio Tinto, BHP, and others) also focus a lot of effort on mining gold and other base metals such as iron ore, nickel, and whatnot. As such, they're not pure plays on copper since a slump in their other businesses would be a drag on copper buoyancy.

Southern Copper does produce some gold and silver, which are often associated with copper mines. And it produces some zinc and molybdenum.

The profits from those other byproduct metals simply help lower Southern Copper's production costs. But copper is by far the primary driver of revenue and profits, which is precisely why Southern Copper is the portfolio ingredient I want—a purer play on the explosive growth of copper demand across the rest of this decade and beyond.

Given the industry's expectation for higher copper prices across 2023 and into 2024, and given Southern Copper's expectation that it will produce more copper this year than it did in 2022, I expect to see the company's revenue to ramp up, which will fatten earnings and drive the share price higher.

Buy Southern Copper (symbol: SCCO) up to $72

Risk Profile: Higher (What does this mean? Before you act, read a full breakdown of my five-level risk assessment scale here.)

Stop/Exit: 55% Trailing Stop Loss

Potential Risks

Although Southern Copper is predominantly owned by a Mexican company, you will find the shares listed on the New York Stock Exchange, which means you'll be able to buy them through any U.S. brokerage firm.

I'm giving these shares a "Higher Risk" rating because this is a commodity play, and commodity prices can be extremely volatile. Moreover, while obvious tailwinds are pushing Southern Copper in the right direction, there are some factors I want you to be aware of:

1. China

There's always the risk that China shutters its economy again because of a dramatic flare-up in COVID. I don't consider this a big risk simply because China and the world have come to grips with COVID and are much more likely to let another outbreak run its course now that vaccines and herd immunity are so widespread. But it's important to note.

2. Central Bankers

Here the risk is that Western central bankers raise interest rates so sharply to tackle inflation that they induce a deep global recession... which in turn would slam the global commodities market as demand collapses. I'm not convinced that happens, but I cannot rule it out, because as an independent, non-governmental body, the Fed doesn't answer to Congress.

The banking crisis that erupted recently certainly reduces this risk, since hiking rates into a series of bank failures would be asinine. But this is the Federal Reserve, so it remains a risk.

3. Social Unrest

This is the primary risk. In fact, it's not uncommon in the mining sector.

Chile and Peru are regularly rocked by social unrest tied to political anger or fights with mining companies. Plus, Peru has been engulfed in a political crisis for several months that has hamstrung transportation, among other effects.

Earlier last year, Southern Copper closed the Cuajone Mine for several months after protestors shut off access to water and blocked a railway line used to transport ore. The protesters were demanding compensation for use of their land.

Because of those protests, production at Cuajone dropped by 17%. Similarly, copper volume dropped by 14% at Toquepala. Those two factors combined to hit Southern Copper's top and bottom lines for 2022.

Net sales of just over $10 billion fell nearly $900 million from 2021's result. Meanwhile, net profits of $2.6 billion slipped by nearly $760 million.

So, clearly, this is a very real risk. Nevertheless, history tells us that the protests die down in time and normalcy returns.

If another protest were to occur that saw Southern Copper's share price decline, I would actually be a buyer in that moment. These crises are always fleeting, yet demand for copper is never-ending.

Moreover, copper is the primary lifeblood of the Peruvian economy, representing 30% of the country's total exports. Which means the government has to protect that copper goose at all costs.

So, if you recognize the risk of social/political unrest exists, and you are prepared to hold fast through any future flare-ups, you can expect meaningful returns from owning these shares.

Potential Rewards

As I write this, the shares are trading in the $68 range. Looking out over the next 18 months to two years, I predict a price north of $100. That's based on per-share earnings of $4 by 2025 (they were $3.05 last year), which would give the company a price-to-earnings (P/E) ratio of 25.

Southern Copper has historically traded at a P/E between the high-teens and 30. So, even a P/E of 25 is likely underplaying the stock's potential as growing global demand for copper flows through the company's balance sheet.

Granted, "north of $100" is not a double from $68, as I mentioned at the outset. The double comes three to five years out, as demand for copper ramps substantially higher.

But as we wait for the shares to pop, Southern Copper will pay us a nice dividend. Last year, that amounted to $3.50 per share, equating to a meaty annual yield of 5.88%, well above the S&P 500's current average yield of 1.65%.

The bottom line here is that copper has an extremely bright future with long-lived demand. Southern Copper is one the best ways to benefit from that trend.

Ted Baumann is International Living’s Chief Global Diversification Expert.

In the late 1970s and early 1980s, legendary investor Warren Buffett began making a series of large, aggressive bets in the stock market.

These bets weren't based on his expectations about a particular company or even a particular industry. Instead, they were based on something much bigger… the future direction of the U.S. government and economy.

The 1970s were plagued by high inflation. Throughout the decade, inflation ranged from 5.5% to a massive 14.4%.

As the end of the '70s approached, Buffett gambled that the government would have to finally tackle this runaway inflation. And once it did, inflation and interest rates would start to fall, which would mean better stock market returns.

Similarly, he bet that voters would punish the ruling, pro-union Democratic Party for failing to manage this crisis… which would bring the anti-union Republican Party back to power.

In other words, Buffett figured that many of the big, overarching trends driving the markets—things like government spending priorities, union protections, the rate of inflation, and the level of interest rates—were about to flip completely, and that this would produce new winners and losers in the economy.

Buffett's reading of the situation was spot-on. And the bets he made paid off handsomely. For example, he invested $500 million in media company ABC in 1985, predicting that lower interest rates would improve its cashflow. Ten years later, Disney bought ABC for $19 billion, handing Buffett a gain of $2.2 billion.

Paying attention to changes in the macroeconomic environment, or "macro regime," helped make Buffett the legend he is today.

This story is pertinent because right now, we're in the early stages of a new macro regime. The political, economic, and investment trends that defined the past decade are shifting radically.

Which means that we, as savers and investors, need to embrace a new way of thinking about the markets and the wider economic and political world.

The Trap of "Recency Bias"

Investors tend to have short memories, by which I mean they often suffer from something called "recency bias." Put simply, this is the tendency to assume the immediate future will look much like the immediate past.

When the stock market is doing great guns, investors assume it will continue. Even when the market takes a temporary downturn, they double down on their bets, remembering how doing so in the past paid off.

It's similar in bear markets. Even when signs of an upturn emerge, investors remain fearful, presuming it's a temporary break from the norm and that markets will soon start falling again.

But sometimes an upturn or downturn isn't temporary. Sometimes it's a deep and widespread break with the past. Or to put it another way, it's the end of one macro regime and the start of another.

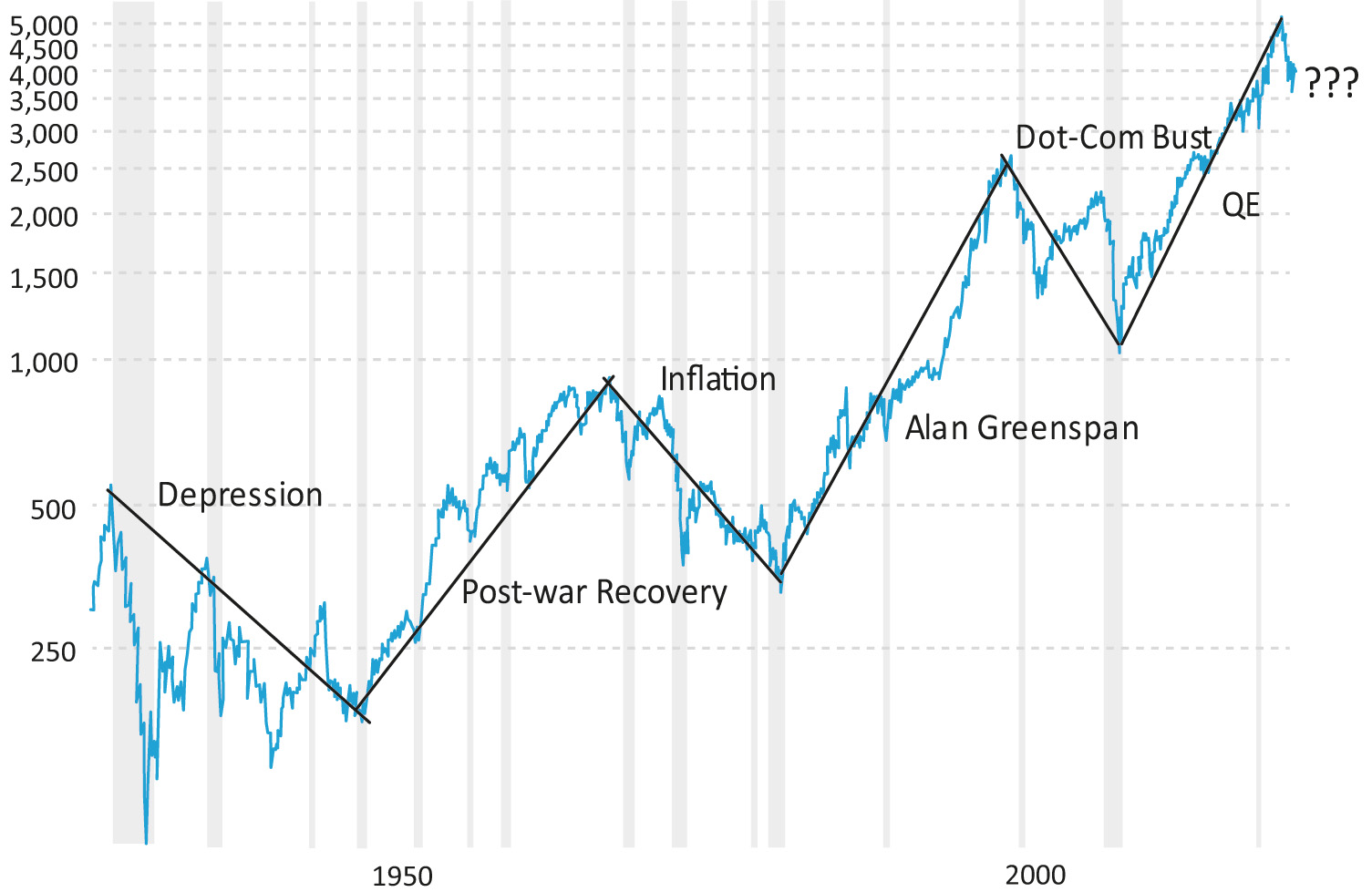

The chart below shows the S&P 500 since the start of the Great Depression. We can see that there have been six macro regimes in that time.

The first, the Great Depression, started with the stock market crash of October 1929. This regime ended after World War II, when the U.S. experienced an economic boom and became the dominant global economy.

Various trends that developed during the post-war recovery—like the increasing power of labor unions and the rise of the military industrial complex—then led to the excessive inflation of the 1970s. This persisted until Federal Reserve Chair Paul Volker boosted interest rates to 20% in 1981, massively tightening the availability of capital.

The next macro regime came after Ronald Reagan appointed Alan Greenspan chair of the Federal Reserve. Greenspan believed in deregulation, and kept interest rates well below their historic norms. Both were good for financial assets. Eventually, however, excessive liquidity and low interest rates led to wild speculation in the early internet era, which resulted in the 1999 dotcom crash.

The most recent macro regime was due to another period of easy money. After the global financial crisis, the Fed and other central banks adopted extraordinary measures to prop up their economies.

This time it wasn't just low interest rates. Major central banks also bought vast amounts of government bonds and other financial assets, a practice known as quantitative easing, or QE. This massively increased the amount of money in the economy, leading to the market boom of the past decade or so.

But now that period is ending… we're entering the seventh macro regime since the Great Depression.

Regime Change in the 2020s

Several years back, when I was working as a financial writer and investment analyst, much of the talk was that the 2020s would be another "roaring" decade like the 1920s. I was skeptical. My analysis of the macro regime suggested that change was in the air, and we were heading for precisely the opposite.

History proved me right—if a bit premature (a common problem for macro analysts). The government's massive COVID stimulus payments helped fuel a market boom in 2020 and much of 2021. I was cautious in the initial stages of this trend, but eventually recommended dozens of stocks that produced triple digit gains for my readers.

But I scored those gains only by recommending that readers sell those positions in the fourth quarter of 2021, when it was clear the macro regime was poised for a shift. Since then, the market has been broadly down (with some notable exceptions).

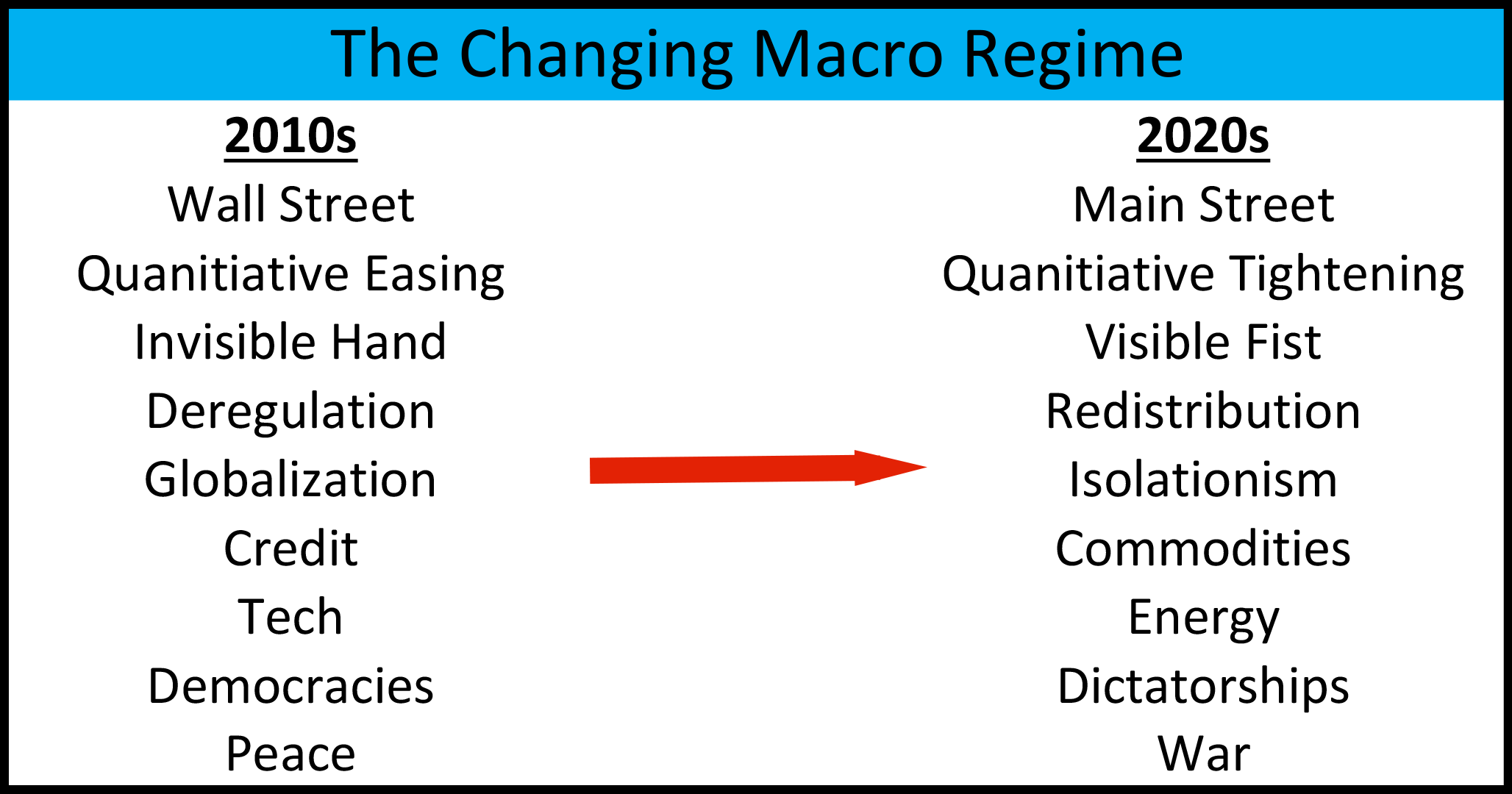

So, what will the new macro regime look like? The graphic below summarizes how the major investment themes are shifting.

The main elements of the new macro regime can be broken down into five main categories.

Reversing Globalization

Probably the most important shift is the end of the "neoliberal consensus" in place since the 1980s… the idea that globalization is universally good.

The globalization of the last 40 years has helped corporations achieve record profits, and consumers enjoy historically low prices for goods. But it has also led to the decline in economic and political status of wage earners in most Western countries.

Outsourcing manufacturing to China and other foreign economies has pushed many voters on the left and right in the direction of populist movements, which demand greater government intervention in the economy.

Main Street, not Wall Street

At a policy level, the end of the neoliberal consensus means a more protectionist approach to global trade, and increased taxation on business and the wealthy. This can be summarized as an emphasis on Main Street rather than Wall Street, and on the "Visible Fist" rather than the "Invisible Hand."

Tightening Money Supply

During the QE period, technology companies tended to do very well. One reason was the success of their products and business models, of course. But low interest rates and abundant credit meant they could amass enormous financial resources to acquire emergent competitors, invest in new technologies… and above all, use predatory pricing to crush competition.

Jeff Bezos deliberately suppressed Amazon's profitability for its first 15 years of existence because he wanted to undercut traditional retail as well as other online competitors. He knew that once he'd achieved that, he could raise prices and reap the rewards of monopoly pricing. Uber used a similar strategy.

Tech companies benefited from QE because near-zero interest rates made "risk-free" investments like Treasury bonds not worth holding. So, money flowed into the stock market instead. That pushed up stock valuations, especially of fast-growing technology companies. However, as we move from QE into QT (quantitative tightening), rising interest rates and higher inflation will see investors return to bonds and commodity stocks, especially energy.

The End of the American Century

As the world's dominant economy after World War II, the U.S. fostered an international order based on low taxation, free capital flows, and fewer barriers to trade. It also encouraged the adoption of democracy around the world.

When global living standards were rising, American economic hegemony was tolerable and even welcome. But after the global financial crisis, people in many countries began to question why they should go along with the U.S.

The number of liberal democracies is now declining. In Europe, countries like Hungary, Poland, and more recently Italy, have adopted nativist right-wing governments that favor reducing the cultural influence of the U.S.

For other countries, the sense that U.S. domination is disintegrating has led to aggressive foreign policy decisions. Russia's invasion of Ukraine is a clear example. China, too, is more antagonistic toward Taiwan. The U.S. will have to beef up its military in preparation for conflict with these challengers.

Permanent Inflation

As countries rush to bring production of goods back onshore, prices will inevitably rise. Rebuilding domestic production capacity requires new infrastructure like manufacturing plants. That will increase costs, which is inflationary.

But the real inflationary elephant in the room is a declining proportion of working age people in developed economies, combined with a reluctance to allow immigration from the rest of the world.

Over the last generation, much of the low-skilled labor in Western economies has been supplied by immigrants, whether documented or not. Anti-immigrant sentiment alongside an aging population means fewer workers... and therefore, higher inflation.

Investing During the New Macro Regime

As the new macro regime takes hold, investment strategies that worked well in recent decades no longer will. Here's what I'm doing with my personal portfolio-steps that could very well work for you too.

I don't have a crystal ball, so I can't predict the future. But as a student of economic history, I can learn from the past. And history tells me that the world we live in is changing rapidly.

■ Why U.S. oil production will never exceed pre-pandemic levels.

One of the factors causing the impending global energy crisis is lower levels of oil production in America.

Back in November 2019, U.S. oil output hit a record high, averaging 13 million barrels per day. Then COVID struck, demand for oil collapsed since everyone was stuck at home, and companies halted a lot of production and stopped exploring for new reserves.

In a very real sense, it was like someone flicked an "off" switch on the entire oil industry.

The problem is the oil industry can't be turned back on quickly or easily, and U.S. domestic production has been recovering at a slow pace.

Despite high oil prices last year, U.S. production in 2022 reached an average of just 11.9 million barrels per day, significantly lagging the November 2019 record. This year, the U.S. Energy Information Agency is forecasting that average production will be 12.4 million barrels per day.

To compound this problem, demand is increasing even as U.S. supply is lagging. This year, global oil demand is expected to be 1.5 million barrels per day above pre-pandemic levels, according to the International Energy Agency.

So, we have soaring global demand combined with domestic supply that remains below pre-COVID figures. And the U.S. energy industry is warning that there's no easy way to resolve this situation…

Earlier this month, Scott Sheffield, CEO of Pioneer Natural Resources, told CNBC that the U.S. would never be able to exceed the 13 million barrel per day average achieved in November 2019.

The U.S. might be able to touch that figure again but wouldn't be able to push higher, he said, adding that even returning to the November 2019 levels would take another two to three years.

A major issue, Sheffield notes, is that the U.S. lacks refining capacity. Refineries have been closing but few new facilities are being built to replace them due to green transition policies.

This is discouraging companies like Pioneer from boosting production, since it would just increase the strain on existing refineries, as well as the fees those refineries would charge.

So, the only solution America has is to buy more oil from the Middle East and elsewhere… which means higher prices.

Put all these factors together and current oil prices in the $80 per barrel range are likely the bottom for this cycle, and we can expect higher prices for oil (and at the gas pump) as the year progresses.

■ These companies are converting real-world properties into investible crypto assets.

One of the most important, but underreported, trends in the cryptoconomy is the rise of tokenized real estate investment vehicles.

These companies take real-world properties and put them on the blockchain (the ultra-secure digital ledger technology behind bitcoin and all other cryptos). This allows the companies to divide the houses into however many shares they want—a process called fractionalization—and then issue crypto tokens to represent those shares.

So, for instance, one of these companies could buy an apartment in Miami Beach for $1 million and add it to the blockchain as 100 crypto tokens. Then, every investor who bought one of these tokens would own 1% of the property and could potentially collect income and capital gains from the rental and sale of the property.

Fractionalization can be managed cheaply and securely with blockchain technology… which means it's a potential game-changer for the real estate investment sector.

The big players in this new industry include HoneyBricks, which focuses on commercial real estate… Arrived , which targets rental homes and vacation rentals… and Roofstock, a major real estate investment marketplace that recently added tokenization to its platform.

Now, to be clear, I'm not endorsing these platforms, since I haven't used them personally. Moreover, this is an emerging industry and the risk to investors is likely high.

But the emergence of these platforms is yet another indication of how crypto technology is quietly transforming the traditional investment landscape.

■ Secondhand luxury watches are the hottest new investment asset class.

In the cover story of last October's issue of the Global Intelligence Letter , I wrote about the rise of collectibles as an asset class and how they would outperform traditional markets in this high inflationary environment.

One of the collectible categories I highlighted in that story was luxury watches and just as I predicted, they've been on a tear of late.

According to a new report published this month by Boston Consulting Group, secondhand luxury watches have been growing in value by about 20% annually since mid-2018. That's more than doubled the pace of the S&P 500, which is up about 8% per year over the same period.

The report found that the watches are particularly popular with young investors, who see them as an inflation hedge and an effective form of wealth diversification.

Nicolas Llinas, who co-authored the report, said the market for luxury watches is so strong at present that collectors are paying two to three times the recommended retail price for certain models as soon as they leave the store. Boston Consulting Group noted, for example, that Rolex Cosmograph Daytona watches with a retail price of $14,800 had sold for as much as $38,500 on secondhand platforms.

This strong demand is also driven by low supply, since many luxury watchmakers shuttered their production facilities or saw reduced output during the pandemic.

Increased supply may lead to a slight moderation in prices, though with inflation set to remain elevated for years to come, I expect luxury watches to continue to see strong demand.

■ You can now sell your online data to private companies… but is it a good idea?

The global advertising industry is in the midst of a huge transition. This began when Apple started allowing users to opt out of some tracking. Now, Google is preparing to ban a type of tracking software called cookies.

For more than a decade, advertisers have relied on these technologies to monitor almost everything we do online. Now they're being locked out. So, they need a solution. And what they've come up with is something called "zero-party data sharing."

Under this model, companies are simply offering to pay users for access to their data.

For instance, a Chicago-based startup called Tapestri is paying users up to $25 per month for access to their location data. The company will then make a profit by selling that data to third parties.

Another startup called Invisibly is granting access to paywalled news articles to users who share demographic and behavioral data, like political affiliation. And an app called Caden plans to give users up to $50 per month in cash if they link their online entertainment accounts like Netflix or Amazon Prime to the service.

It sounds like a nice deal… Get paid up to $50 per month without having to do anything or change your behavior in any way. But of course, there's no such thing as a free lunch.

The problem with these services is that it's difficult, or impossible, to learn which organizations they're selling the data to. They're likely selling to advertisers, but could potentially be selling to government agencies, your employer, even law enforcement. Until we get more clarity on this emerging industry, I'll be keeping my personal data private.

■ Visit 135 countries in three years for less than the cost of renting an apartment in New York.

A company called Life at Sea Cruises has announced its first-ever three-year cruise. Under the plan, the ship, MV Gemini, will travel to 135 countries on seven continents and stop in 375 ports of call over the three-year period. Each port-call is expected to last several days to give passengers a chance to explore the destinations.

The ship comes equipped with the usual entertainment options, but also offers a business center and private offices for those who want to work during the voyage. It even has a 24-hour hospital.

And the cost for all this? Prices start at $29,999 per year, or $2,499 per month including food and lodging. Considering that Zillow lists the median rent for an apartment in New York at $3,300, it's not a bad deal at all.

That's not to say I'll be signing up, however. Personally, I think I'd get severe cabin fever after more than a month or two aboard a ship. Still, in this new age of remote work, this cruise package demonstrates the growing demand for new and more interesting lifestyle options.

■ Spring is the worst time to buy… pretty much anything.

Spending on all manner of outdoor and household goods is depressed in winter, since people are loath to fight their way through snow and rain just to get a new toaster or couch or TV.

However, when spring arrives, people start heading outdoors… and opening their wallets. Stores know this, which is why the prices for all sorts of items peak in spring.

Patio furniture, grills, home furniture, televisions, computers, office supplies, exercise equipment, summer clothes… the prices for items in all these categories and more spike to their highest levels around this time of year.

That's why, if you're in the market for any of these items, it's best to wait until June or July, or at least the Easter sales, before splashing any cash. Once the season is winding down, the prices of these items will fall significantly.

■This might be the ultimate time-saving tip.

Few things are more infuriating in life than trying to explain how to fix a tech-related issue over the phone… particularly to an elderly relative who's less than tech-savvy.

Now there's an easier way. You can remotely take control of their computer from anywhere in the world using your own device… and it won't cost you a dime.

Here's how to do it…

On a Windows device, open your Windows search bar and search for a tool called Quick Assist. When you open the app, it will give you the options to "Get Assistance" or "Give Assistance."

Click on "Give Assistance," log in to your Microsoft account, and you'll get a security code. Give this to the person you want to help, ask them to input it into the Quick Assist app on their Windows device, and hey presto, you'll be able to remotely control their computer. Now, you can quickly and easily fix the problem on their machine by yourself.

On a Mac, the easiest way to do this is to open the Messages app and start or continue a conversation with the person you want to assist. In the top right-hand corner of the screen, you'll see the information icon (a lower case "i" in a circle). Click this and you'll see the option to share screen. Select this and select "Ask to Share Screen." With that, you can remotely control the other person's device. It's that easy.

These settings are an amazing time-saver if you're the go-to person for tech support in your extended family or friend group.

■Don't ignore this unfairly maligned super food.

Scientific guidelines around food have changed a lot since we were young. Nowhere is this more apparent than with eggs.

Eggs contain tons of cholesterol, or about 200 milligrams in every yolk.

For this reason, major health advocacy bodies, including the American Heart Association and the Office of the Surgeon General, spent decades advising Americans to eat fewer than three eggs per week.

But it turns out, that advice was entirely wrong.

We now know that the cholesterol contained in foods, and the cholesterol in our bloodstreams that clogs up our arteries, are only weakly related. And eating one does not necessarily lead to a big increase in the other. Moreover, eggs are packed with protein and nutrients like vitamin D.

So, since 2015, the government's Dietary Guidelines for Americans contain no specific limit on how many eggs you can eat. In fact, the Food and Drug Administration says eggs can be labeled a health food, and the American Heart Association now says older adults with normal blood cholesterol can safely eat one or two eggs per day.

Thanks for reading, and here’s to living richer.

Jeff D. Opdyke, Editor

Global Intelligence Letter

© Copyright 2023. All Rights Reserved. Reproduction, copying, or redistribution (electronic or otherwise, including online) is strictly prohibited without the express written permission of Global Intelligence, Woodlock House, Carrick Road, Portlaw, Co. Waterford, Ireland. Global Intelligence Letter is published monthly. Copies of this e-newsletter are furnished directly by subscription only. Annual subscription is $149. To place an order or make an inquiry, visit www.internationalliving.com/about-il/customer-service. Global Intelligence Letter presents information and research believed to be reliable, but its accuracy cannot be guaranteed. There may be dangers associated with international travel and investment, and readers should investigate any opportunity fully before committing to it. Nothing in this e-newsletter should be considered personalized advice, and no communication by our employees to you should be deemed as personalized financial or investment advice, or personalized advice of any kind. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before our subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after on-line publication prior to following an initial recommendation. Any investments recommended in this letter should be made only after consulting with your investment adviser and only after reviewing the prospectus or financial statements of the company.