Dear Global Intelligence Letter Subscriber,

In the spring of 1984 and newly turned 18 years old, I skipped class one morning at Louisiana State University.

I drove the 80 or so miles from the LSU campus to downtown New Orleans—to the only office in the region for discount brokerage firm Charles Schwab & Co.

Though the discount stock brokering industry had begun in 1975, it was still largely a novelty when I opened my first brokerage account with $2,000 that I hand-delivered in the form of a personal check, one of the first checks I’d ever written.

Schwab at that point had just 40 offices across the US—less than one per state.

In short, I was something of a pioneer even though the industry was already nine years old.

Days later, after the check cleared and my account was officially funded, I called Schwab’s toll-free number from an old “Slimline” push-button phone I had in my bedroom and, using those little square buttons on the handset, placed my very first order to buy my very first shares of stock.

That purchase: Flying Tiger, the air-freight company that spun out of the World War II Flying Tigers fighter unit that helped China fend off a Japanese invasion. Back then, I saw that overnight air cargo would emerge as a massive industry and that Flying Tiger would be a player in that. (It was… and was snapped up by Federal Express in 1988.)

I share this anecdote because it highlights the way that technology brings newcomers into newly emerging financial services sectors.

I was never going to open a brokerage account at Merrill Lynch, E.F. Hutton, or PaineWebber, the big brokerage firms I knew of back in the day. (“When E.F. Hutton talks, people listen.” Remember that TV commercial catchphrase?)

I couldn’t afford the huge commissions of hundreds of dollars per trade. Moreover, none of those firms cared about a college freshman with a measly $2,000 to invest.

Nevertheless, the little guy like me had an option to stake my claim on America’s business future by way of Schwab, which, at the time, imposed a flat $35 trading fee. That, I could afford.

When Schwab and the other discounters emerged, they were seen as the “future of stock brokering,” though the entrenched incumbents and their sycophantic adherents vehemently (and wrongly) disagreed. Discount brokers were just a venue for the hoi polloi to lose their money gambling. They were certainly never going to attract the truly moneyed elite who demand personalized services and want access to Wall Street research.

How’d that work out?

When was the last time you heard the name “Merrill Lynch” in any conversation or in any TV ad? I’d bet it has been a dozen years or more, given that Merrill Lynch ended up inside Bank of America during the 2008 financial crisis. American Express bought E.F. Hutton in 1988 and the remnants of what was once America’s #2 brokerage firm has bounced around ever since. PaineWebber, meanwhile, is now UBS Wealth Management, which isn’t even a brokerage firm.

But look at what has become of the discount brokerage industry.

Schwab, Fidelity, E*Trade, Robinhood, TD Ameritrade, Interactive Brokers… they’re the most popular stock-market trading platforms in America, and every last one of them is a discount broker.

The future arrived that the discounters promised. Discount brokers would one day come to rule the roost, and the traditional model of high-cost stock brokerage died away.

Now, we sit on the cusp of another major “the future of” moment.

The future of money.

That future is crypto.

Many—many!—continue to vehemently (and wrongly) disagree with that statement. Physical currency has been humanity’s go-to option for more than 2,500 years. As for the US dollar, specifically, it has served as the world’s most important currency for more than 80 years and as America’s money since 1785.

To think that anything will come along and knock physical money—especially the dollar—off its perch is ludicrous and laughable… at least according to dollar sycophants and those who are preternaturally conditioned to disregard anything that challenges the status quo. They believe that what is will always be, even though the entirety of history proves that their unmovable belief system is wrong.

Truth is, digital money has already changed the world.

Of all the US currency that exists, just 10% of it is actual physical bills and coins. The other 90%? All digital entries on digital ledgers somewhere.

So, technically, we’re already 90% of the way toward a digital money world. The only question is, how soon does that last 10% go digital too?

Once that happens—and it will, 100% guaranteed—the leap from digital fiat currency to cryptocurrency is just a function of governments deciding that in the move to crypto they can monkey with today’s extreme levels of Western debt to find a way to minimize or erase some or most of their obligations.

But monkeying with debt is a different story.

Instead, the story I want to share with you this month is the story of a cryptocurrency that’s shaping up to be one of the most important in the world... and why getting in now means you’re likely to see your investment 5x or more from here.

But before I dive into my specific recommendation, I want to step back and explain crypto for those who are new to the notion, or those who don’t understand why something you cannot see—a cryptocurrency that only exists in the digital ether—is worth anything at all.

Let’s start with the “cannot see it” concept, since it’s so easy to dismiss.

Is a dollar in your bank account worth anything?

Of course it is.

But you cannot see it. As I noted a moment ago, 90% of America’s currency does not actually exist. It’s digital. If everyone today decided they wanted to hold their physical dollars as cash and stuff it under their mattress, the US banking system would fail because there are simply not enough units of physical currency to meet that demand.

Or what about those mutual-fund shares you own in your (discount) brokerage account?

They’re a digital book entry, since mutual funds don’t issue physical shares that you can hold onto.

Much of your financial life, then, is actually digital money. Many people just don’t recognize that fact because they hold dollar bills in their wallet… and they’ve probably seen an old stock certificate in a parent’s or grandparent’s safe or safe-deposit box.

Nevertheless, our financial lives are digital.

Pay for groceries at the local Piggly Wiggly and, I’ll wager, you’re pulling a debit card out of your wallet to scan at the point-of-sale machine. That money automatically leaves your bank account as a debit and magically appears as a credit in the supermarket’s bank account. No one touches any physical currency anywhere in the process. (And if you used a credit card, well, there’s just one extra step in the process—you paying your credit card bill, probably online, meaning another digital touchpoint.)

Cryptocurrency really is no different on that point.

Sure, you cannot see it, but it has value, just as the dollars and mutual funds you cannot see have value.

As for the bigger question, “What is crypto?”, well, the simplest answer is that crypto is a digital financial asset that exists on a blockchain. But that word “blockchain” is where people generally get lost.

Technically, a blockchain is nothing more complicated than an electronic network on which transactions are recorded. But even that seems amorphous. So, think about it as a digital ledger, much like an Excel spreadsheet. And imagine recording every transaction in your daily life on that spreadsheet, without fail.

This “spreadsheet” has three unbreakable rules:

A visual representation showing interconnected “blocks” of data in a blockchain. © iStockPhoto.com/VectorMine

But, you might rightly be wondering, “Why do we even need a blockchain when we already have digital networks that move money around?”

Several reasons:

“Any technology that allows business to collect greater profits, faster, and to create novel products that attract more and new customers… well, that’s a technology that is 100% certain to see mass adoption.”

I joke regularly in my crypto presentations at conferences that the internet did not explode into what it is today because humanity needed a better way to share cat videos. It became the internet we know and rely on in our daily life because business saw a novel path for cutting costs, speeding up transactions, and creating new and never-before-seen products and services.

In short: the internet made business more efficient, meaning it made business more profitable.

And that is precisely what crypto and the blockchain offer… efficiency in the form of radically improved speed, massively cheaper costs, and a venue for creating new products and services that consumers and businesses have never seen until now.

One quick example: A New York company called Parcl Labs has created a financial product in which every new real estate listing, every sale, and every price change in a specific Metropolitan Statistical Area is captured and turned into a “price per square foot” number for that MSA.

Parcl updates and tracks that number every single day. There’s no way to easily do that in the real world. But on the crypto-based blockchain, Parcl can gather up all the data immediately because of underlying technology. Wall Street traders are already using Parcl.

As such, there’s simply no way that crypto doesn’t explode into “the future of money,” because any technology that allows business to collect greater profits, faster, and to create novel products that attract more and new customers… well, that’s a technology that is 100% certain to see mass adoption.

Though more than 10,000 crypto projects pack the cryptoconomy, one project in particular has, in my estimation, one of the brightest futures: Solana.

And that’s where we’re going to be putting our money to work this month.

I’m certain you’ve heard the name. It’s widely mentioned in the press and I regularly write about SOL, as it’s known, in my daily Field Notes e-letter. And to be clear, I am not implying that Solana has replaced bitcoin as “most-favored coin.” Both exist side-by-side. Bitcoin because it’s a long-term store-of-value—a form of digital gold—that will continue to march toward a $1 million price tag before this decade is out, as the US dollar continues its un-halting march south.

Solana, meanwhile, is already shaping up as the cryptocurrency that will, I suspect, become the backbone of our daily spending infrastructure (and I will explain more about that in just a moment).

For transparency’s sake, I’ll tell you that I’ve been part of the Solana ecosystem since the fall of 2021, about a year after Solana launched. I regularly attend Solana conferences around the world, I talk to and write about Solana teams and their projects all the time, and I do some writing for a crypto magazine that is heavily focused on Solana.

Some of my crypto conference name badges, including for the Solana Breakpoint conference.

As I’ve said, I write about Solana often in Field Notes… and I even recommended Solana in the Crypto Strategy Report I put together for you last year.

But I have never given you a complete case for this coin here in Global Intelligence, or officially added it to our portfolio. That changes with this issue.

Solana is one of the top five cryptocurrencies in the world, based on market capitalization, or the combined value of all the Solana coins that exist.

The project launched in 2020 with the aim of addressing speed and cost in the cryptoconomy (and, in turn, in the wider economy).

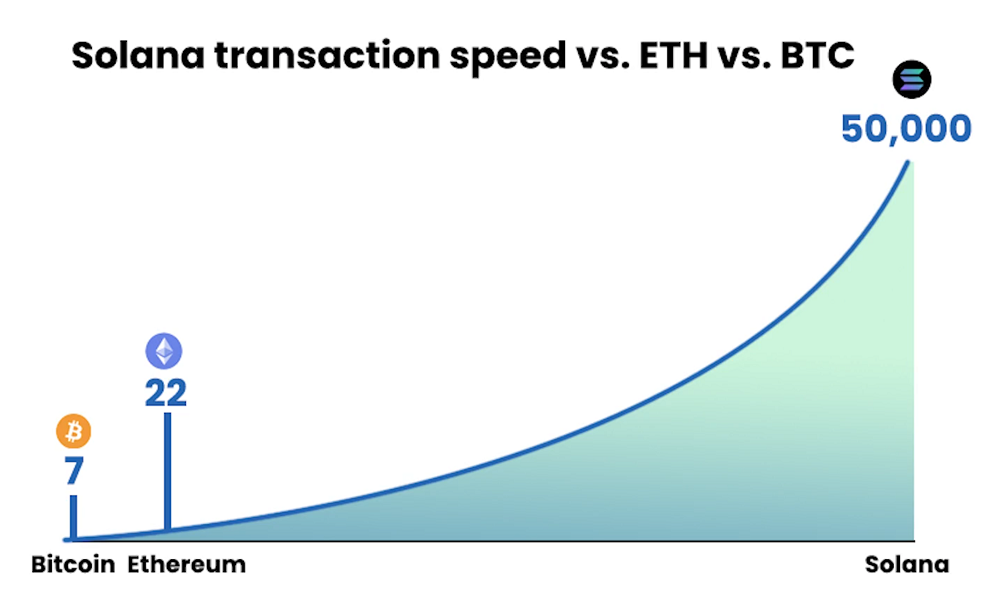

For years now, the two largest cryptocurrencies in the world have stayed the largest: Bitcoin at #1, Ethereum at #2.

Both have humungous global followings. But both also suffer from a speed and/or cost issue. Bitcoin, for instance, processes between 3.5 and 7 transactions per second, at a cost of tens of dollars per transaction. Ethereum is running at about 15 to 17 transactions per second. Costs that were once tens or even hundreds of dollars per transaction are now down to less than a dollar after a series of upgrades. (Depending on network congestion, ETH fees can still spike to tens of dollars.)

As for Solana… as I write this, the network is processing more than 4,000 transactions every second—and theoretically can accommodate 50,000. To put that in perspective, the Visa network on which a global credit-card systems function, processes about 1,700 transactions per second. And the cost of transactions on Solana? About 3 cents or less.

But that’s soon to change.

Solana until recently has had a theoretical limit of 50,000 transactions per second… already much faster than bitcoin, Ethereum, or even the Visa network. But a new upgrade will 20x Solana’s power.

“Solana this year is expected to roll out an upgrade that will make the network capable of operating at 1 million transactions per second. Nothing in the modern financial world moves at such speed.”

Solana this year is expected to roll out an upgrade that will make the network capable of operating at 1 million transactions per second. Nothing in the modern financial world moves at such speed.

The technology behind the upgrade has already been proven in testing, and it’s already working in limited fashion on Solana’s so-called mainnet, where all the daily Solana transactions happen. In fact, not long ago I was scanning the Solana blockchain and captured a moment when the developers were clearly working on something because transactions per second topped more than 96,000.

At a million transactions per second, companies all over the world are going to be interested in incorporating Solana’s network into their business because of the speed and cost savings they’ll achieve. I’m talking about:

Those represent just a tiny, tiny taste of what’s coming. And Solana will help bring all of that to our daily reality when transactions are so fast that a million can occur in a single second.

Already Solana has begun to attract major names, including Visa, PayPal, Shopify, Stripe, Meta, Google, and others that are now looking to incorporate Solana’s blockchain into their operations. Moreover, developers are flooding into the Solana ecosystem these days at a rate faster than on Ethereum, the #2 blockchain. That’s a glaring indication that Solana has emerged as a more attractive platform for building out the products and services that will remake our lives the same way that the internet itself remade our lives starting in the early 2000s.

In short, I expect that Solana will emerge as the most important daily-use blockchain for consumers and businesses.

Here’s what I mean by that…

The financial services industry is rapidly moving toward blockchain technology as its back-office infrastructure. Right now, if you stop into a gas station for a fill-up and a Slurpee, you tap your debit card and machinations begin that traverse the traditional finance world, pulling money from your bank account and depositing it, days later, into the merchant’s bank account.

In a blockchain world, that same transaction happens exactly the same for you and the merchant, at least outwardly, meaning the process of paying for gas and a Slurpee looks identical.

Behind the scenes, however, it’s very much different. The entire transaction happens on the blockchain. It’s more secure than current technology. It’s less expensive. And it’s magnitudes faster in that money leaves your wallet immediately and immediately lands in the merchant’s wallet; the current technology requires days for a transaction to fully complete.

“You’ll soon be buying and selling stocks, bonds, commodities, currencies, even houses, on the blockchain.”

But the changes to the financial world now emerging will go far beyond buying gas and a Slurpee at a mini-mart. Fidelity, BlackRock, and others are looking to move all assets onto the blockchain, meaning you’ll soon be buying and selling stocks, bonds, commodities, currencies, even houses, on the blockchain. That trading will happen 24/7/365, rather than during prescribed, weekday hours.

Robinhood, the discount-brokerage smartphone app, recently announced it’s looking at Solana to help facilitate a project that will allow European retail investors to trade US stocks as “tokenized assets.” Translation: Robinhood will allow everyday investors in Europe to trade Apple, Microsoft, Merck and all the other US stocks as blockchain-based digital tokens.

Doing so would reduce costs because it eliminates the middleman between investors and the stock market. It also reduces trade-settlement times to seconds or hours instead of days.

This is the world we’re rapidly racing toward—one in which everything we do in our personal financial lives will happen on the blockchain. You and I won’t necessarily be aware of that. And we won’t necessarily care. Our debit and credit cards will work the same as always. We’ll be buying the same stocks and bonds and mutual funds. We’ll save our money the same way, though we will have far more options.

The only difference is that, behind the curtain, all of our transactions will occur on the blockchain—at far faster speed, far cheaper costs, and far more securely.

And Solana is going to be one of the most important blockchains bringing this vision to fruition. Behind the scenes, everything will be running on the Solana network, even if you’re paying for that Slurpee or buying stocks or whatever using your regular ol’ fiat-currency credit/debit card and bank account.

So, why do we want to own the Solana coin?

Demand for the network means demand for the coin. The coin is the operating currency of the network. Fees that users pay to operate on the blockchain are paid in Solana. For instance, I’m active in a digital horse-racing game called Photo Finish Live, and every time I add money to my digital wallet, I’m paying a small fee of a few cents. That fee is denominated in Solana, meaning I need to own Solana in my wallet.

Apply that concept to hundreds of millions if not billions of transactions per year once Solana is running at a million transactions per second, and soon enough we’re talking about a lot of people and a lot of companies that need to own Solana in their wallet to facilitate all those transactions.

That demand will drive Solana’s price higher over time.

Because SOL is one of the most heavily traded cryptocurrencies globally, you can find it trading on every major and minor crypto exchange in the world. Plus, you’ll find it available on PayPal, as well as brokerage firm apps including Robinhood and Webull.

I use Coinbase, one of the world’s largest crypto-specific exchanges (Coinbase just recently joined the S&P 500 as the first crypto company to be included in the index). Other exchanges including Kraken and Gemini as equally as good.

If you don’t have a crypto-exchange account, you can follow the directions in this special report starting on page 17. It will walk you through the process to create a Coinbase account.

I would also tell you to consider setting up a dollar-cost averaging plan and putting your money to work over the next month or two. I’ll use Coinbase as an example of the process:

The reason I suggest this approach stems from Solana’s volatility (we’ll get to that soon) and my recommendation that you buy SOL up to $200.

SOL’s price is guaranteed to bounce around like a Super Ball. It might cross $200, it might dip to $120. Impossible to say. This is crypto—and wild swings come with the territory, like any new asset class. (I explained a little more about why crypto swings wildly, right here.)

So instead of trying to guess, “Is this a good time to buy? Or should I wait? Will I miss out??” just set up a recurring buy and don’t fret about price. You’ll build your position, and you’ll likely have a better overall entry price.

Because this is a double-issue of Global Intel, I’m also giving you a second way to play Solana’s future… and it’s especially for you if, for whatever reason, you don’t want to own crypto directly and prefer to play the stock market.

In this case, I’m recommending you own a stock called SOL Strategies.

The company began years ago as Cypherpunk Holdings, which invested in technologies aimed at enhancing or protecting online privacy, particularly within the broader blockchain ecosystem. However, last fall the company shifted its focus to concentrate on owning and investing in Solana.

Today, Toronto-based SOL Strategies’ purpose is to buy, own, and “stake” Solana in order to earn an income.

Staking, I know from many a conversation, is not a term most investors are familiar with, so let me explain. In simplest terms, imagine depositing cash into a certificate of deposit at your local bank. Your money helps secure the bank in that it’s the money the bank uses to lend out to borrowers, who then pay interest to the bank, which is how the bank generates an income to keep the lights on.

In return, the bank pays you a fee—an annual interest rate—for keeping your money on deposit.

In the crypto world, staking is akin to a deposit. You stake (deposit) your crypto coins (cash) and earn an income.

The stacking happens not at a bank but with a “validator.”

These are computers, owned by individuals all over the world, running software that, in turn, runs the Solana blockchain. These computers process, verify, and validate every transaction that occurs and, in so doing, build the Solana blockchain. Going back to that imagery of children’s blocks earlier in this issue, validators are basically building those blocks, ensuring they’re legitimate and secure, and then Gorilla-gluing them into place so that no one can ever go back and mess around inside that block or move it around in the blockchain.

The way the Solana network works, validators need a certain amount of the Solana coin to power the process. (There’s more to it than that, but I don’t want to bog you down in blockchain philosophy and boring details.)

The nut of all of this is that by staking Solana coins with a validator, an investor is helping secure the blockchain. And for that, they earn an income, paid out in the form of additional Solana tokens. Validators—and, thus, those who have staked their coins with a validator—also earn part of the fees that blockchain users pay when conducting their transactions. By way of example, I’ve got my Solana staked with a particular validator and I’m earning about 7.33% per year at the moment.

SOL Strategies is doing this on an industrial scale.

The company owned nearly 140,000 Solana coins as of the end of last year, according to SOL Strategies’ latest quarterly financial reports. All of those are staked with three validators that SOL Strategies runs itself (anyone can be a validator with the right equipment).

In turn, those staking/validator operations earned SOL Strategies $1.24 million in staking income. It’s also earning revenue by allowing others stake their Solana through SOL Strategies’ validators.

Annualizing the company’s fourth-quarter efforts, which represent the first full quarter of operations in SOL Strategies’ current form, combined revenue from staking and validator fees is nearly $14 million. A year earlier, that figure would have been less than $300,000.

As the income starts to flow in, the company will begin looking to put some of it into other investments in the Solana ecosystem to create new revenue streams. Management has stated that it’s also looking to enhance its revenue by launching validators in Europe and Asia, and to attract institutional clients to its validators, such as Solana ETFs—which are set to be approved soon by the SEC—which would allow the ETFs to earn an income for their investors.

In essence, SOL Strategies is shaping up as the Solana version of Microstrategy, now known simply as Strategy, the tech company run by bitcoin super-bull Micheal Saylor. Though Strategy’s original business is providing business-intelligence software, the company has become known almost exclusively for its corporate treasury, which owns 576,000 bitcoins, worth nearly $65 billion. As bitcoin’s price goes up, Microstrategy’s stock price rises as well.

SOL Strategies offers a very similar play on Solana.

As the price of Solana rises, and as SOL Strategies increases the amount of Solana it has staked and the amount of Solana others stake with the company’s validators, the company’s income will rise... meaning the share price will rise too.

And as a potential stock-price sweetener, SOL Strategies is seeking a listing on the NASDAQ Stock Market in the US.

Right now, the company is fairly well hidden away in Canada, and not all US mutual funds can trade Canadian shares. Moreover, very few Americans pay attention to Canadian stocks, particularly tiny Canadian stocks, so SOL Strategies is well off the radar in the US.

But once the stock trades on NASDAQ, the number of potential buyers increases sharply. That, in turn, could lead to increased demand for the shares and, thus, a richer stock price.

I am not basing any part of my investment thesis on a NASDAQ listing, but it would nevertheless benefit shareholders if it happens.

As I write this, SOL Strategies is trading at $2.86 per share, so you have some room to operate before hitting the buy limit.

As I noted, SOL Strategies is a Canadian company. But the prices I’ve given you are in US dollars and the stock symbol I’ve listed is for the US shares that trade in the “over-the-counter” market. Daily trading volume is regularly over 1 million shares, and has hit 5 million on occasion, so you should have no problems building a position.

The one challenge you might face is access to the stock. Not all the app-based brokerage firms allow trading in foreign shares. Some do, some don’t. So, if you’re using one of those platforms, you will need to check on availability.

But you should have no issues trading on traditional discount-brokerage sites such Fidelity and elsewhere.

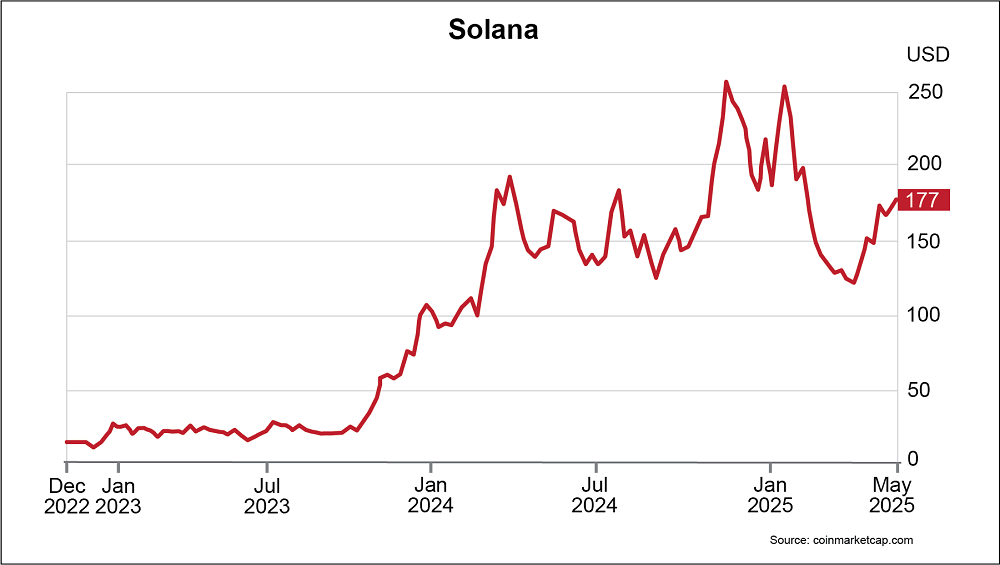

As I mentioned, crypto prices can move up and down by large amounts and with numbing velocity. Solana is a great example. SOL’s price raced from less than $10 per coin in late 2022 to nearly $300 early this year… only to sink to $95 in April… which then sparked a rally back above $180.

It’s about $167 as I write this.

I called the bottom on Solana in January 2023, and it’s had an amazing price run-up since then. But we’re still early in SOL’s story—and it’s still a good time to buy. (The chart shows end-of-day prices; but even during any given day, prices can bounce considerably.)

You absolutely must know that you have a cast-iron stomach before you act on this recommendation. I can guarantee that Solana’s price will whipsaw.

If you make this trade, I do not want you to get pushed out of the position because a temporary decline triggers an arbitrary stop-loss order. Nor do I want you to push yourself out of a position in Solana because of personal nervousness at the red ink you see.

You really do have to go into Solana (or any crypto) knowing that you’re only putting at risk an amount of money you absolutely can lose without disrupting your life… and that you are not going to sell out in knee-jerk panic when the price plunges (temporarily) on some exogenous factor like events in the news.

We’ll be looking to hold SOL for a few years, though I will recommend selling half your position at a 100% gain, when we reach that.

My ultimate price target is $450 to $500 per coin during this bull-market cycle, which I expect to continue till, say, the end of 2026. (In a blow-off top tied to a crazy bitcoin price runup, SOL could see $600 or more.) Moreover, the US Securities and Exchange Commission is in the process of likely approving the first Solana-based exchange-traded fund. When that ETF is launched, we’re absolutely going to see a mad rush of institutional money into that fund because so many institutions can’t, or don’t want to own cryptocurrencies directly through digital wallets.

“SOL could hit $1,000 as the Solana blockchain emerges as the backbone of daily finance.”

Longer term (end of the decade), I have a $1,000 target on SOL as the Solana blockchain emerges as the backbone of daily finance.

As for SOL Strategies’ risk rating… well, this is purely a crypto company, so it has the same risk as Solana itself. Moreover, this is a small public company, so we face traditional corporate risks like bankruptcy, idiotic diversification efforts, etc. I am not saying that’s a strong likelihood with SOL Strategies, but it is a risk with companies that are this small. (The market cap is less than $500 million, so it’s just barely above a micro-cap stock.)

As with Solana itself, if volatility is going to cause you to panic about losing your money, then I urge you to stay away from this one.

If, however, you fully understand that this investment will bounce around—possibly wildly—then owning some exposure to SOL Strategies could pay off big. Back in late 2022, you could have bought Microstrategy for just over $13 per share. Today, it’s above $400.

I am not predicting a similar trajectory for SOL Strategies, but I am predicting that as Solana heads higher, SOL Strategies will do very well.

Though Solana’s price is up markedly from when I called the bottom near $20 per coin back in January 2023, we are still so early to this game. Solana recently reported that there are now more than 11 million Solana digital wallets—a big number in Solana terms, but a miniscule number relative to the global population.

It points to the fact that mainstream adoption, which is clearly on the upswing, has not really happened yet.

So imagine Solana’s price when it’s not 11 million wallets that the blockchain is celebrating… but 100 million or 500 million. Or even 1 billion.

Like I said, we are so early.

Which is why Solana is, for me, a buy-and-hold investment. You pack it away in your portfolio… you continually add to it on dips, or you simply set up a dollar-cost averaging plan and buy it regularly from now until forever… and one day you’re going to find that you’ve built a pile of wealth that exceeds your expectations.

That’s Solana.

That’s the future of money.

Since this month’s main story centers on the Solana cryptocurrency, I figured this month’s portfolio review would serve as a fine opportunity to detail what’s up these days in the crypto market overall.

As I write this, bitcoin has recently touched a new all-time high of just over $112,500. As recently as early April, the grandaddy of crypto was as low as $74,400, after hitting its previous all-time high just over $109,000 back in January.

That rollercoaster—down 32% then up 51% in a span of four months—speaks to the market of the moment.

As 2024 ended and 2025 began, the cryptosphere was agog with the euphoria of a Trump presidency and his promises to make America the “crypto capital of the planet.” That euphoria propelled crypto prices higher and sent bitcoin to its January peak.

Alas, Trump has not—yet—followed through with much of the crypto platform that he promised, which has left the so-called “crypto bros” feeling bent out of shape… and bent out of shape crypto bros are very fickle animals who simply dump their holdings rather than demonstrate even a modicum of patience. Hence why we are not—right now—seeing higher and higher highs.

Nevertheless, the ongoing bull market never went away.

We remain firmly entrenched in what I suspect will prove to be the Mother of All Bull Markets, as I wrote about in your Global Intel issue on bitcoin last year.

We continue to see vast institutional uptake of crypto.

The iShares Bitcoin Trust ETF, which launched in January 2024, has about $70 billion under management. The world’s largest gold ETF, the SPDR Gold Trust, has just $97 billion under management—yet it has been around for 21 years. Clearly, vast sums of money are flowing into bitcoin, and quickly.

Moreover, as I’ve noted several times in my daily Field Notes e-letters, countries all over the world, and states all over the US, are in the midst of building bitcoin reserve funds. The Texas legislature, for example, recently approved a bitcoin fund and Texas Gov. Greg Abbott has indicated he will support the legislation when it gets to his desk for a final signature.

My point is that crypto is moving into an entirely new age.

For the entirety of its existence, crypto was a fringe asset—to some, it remains a scam and a Ponzi scheme.

But to the world at large, including global governments, bitcoin in particular and crypto more broadly, is emerging as a must-own asset class for two reasons: growth opportunity and, more importantly, protection against the ongoing destruction of wealth held in Western currencies.

The dollar in particular faces intense headwinds because of extreme American debts, relatively high interest rates that now force Uncle Sam to shell out more than a trillion dollars per year in interest costs, and an increasing amount of fear among foreign investors who are abandoning US assets, including the dollar.

Bitcoin is the insurance policy.

And where bitcoin goes, so goes the rest of crypto… ultimately.

I emphasize “ultimately” because bitcoin doesn’t raise all tides equally or at the same time. Typically, bitcoin goes up, and then investors begin to focus on secondary leaders such as Ethereum, Solana, and others.

That’s where we are right now. Bitcoin is going up and the others are kind of lagging. They’re rising, but in a much choppier fashion. Solana, for instance, is up 80% in just a few weeks, but remains 70% off its January record high. Ethereum is 80% below all-time highs it set back in 2021.

As such, we’re in a really good moment to be a buyer of high-quality crypto assets, particularly Solana.

And that, aside from anything else, is why I’ve officially added it to our portfolio this month.

Thanks for reading, and here’s to living richer.

Jeff D. Opdyke

Editor, Global Intelligence Letter

© Copyright 2025. All Rights Reserved. Reproduction, copying, or redistribution (electronic or otherwise, including online) is strictly prohibited without the express written permission of Global Intelligence, Woodlock House, Carrick Road, Portlaw, Co. Waterford, Ireland. Global Intelligence Letter is published monthly. Copies of this e-newsletter are furnished directly by subscription only. Annual subscription is $149. To place an order or make an inquiry, visit https://internationalliving.com/page/faq/. Global Intelligence Letter presents information and research believed to be reliable, but its accuracy cannot be guaranteed. There may be dangers associated with international travel and investment, and readers should investigate any opportunity fully before committing to it. Nothing in this e-newsletter should be considered personalized advice, and no communication by our employees to you should be deemed as personalized financial or investment advice, or personalized advice of any kind. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before our subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after on-line publication prior to following an initial recommendation. Any investments recommended in this letter should be made only after consulting with your investment adviser and only after reviewing the prospectus or financial statements of the company.